On June 13, 2025, Israel launched a series of large-scale military strikes targeting Iran’s nuclear facilities, military infrastructure, and key personnel, escalating tensions in the Middle East to unprecedented levels. The attacks, which Israel described as a preemptive measure to curb Iran’s nuclear ambitions, killed senior military commanders and nuclear scientists, damaged critical infrastructure, and prompted Iran to retaliate with missile and drone barrages aimed at Israeli territory. This intensifying conflict has sent shockwaves through global markets, particularly the fertilizer sector, where Iran’s role as a major supplier of nitrogen-based fertilizers like urea has drawn heightened attention to wartime premiums and potential supply chain disruptions. The implications of the Israel-Iran conflict may have a ripple effect on the global fertilizer market, from the economic, logistical, and geopolitical standpoint, factors that may be drive wartime premiums.

The Middle East’s Critical Role in the Global Fertilizer Market

The Middle East is a powerhouse in the global fertilizer industry, particularly for nitrogen-based fertilizers such as ammonia and urea. In 2016, the region accounted for an estimated 17 million tons of ammonia production and 22 million tons of urea production, making it one of the largest producers globally. Iran, alongside Qatar and Saudi Arabia, is a leading exporter, with Iran alone responsible for approximately 16–17 million tons of urea exports annually, making it the world’s third-largest urea supplier. The region’s competitive advantage lies in its abundant natural gas reserves, a key feedstock for nitrogen fertilizer production, which allows for low-cost production and export-oriented operations.

Iran’s fertilizer industry is particularly significant due to its strategic location and robust export capacity. The country’s urea exports primarily serve markets in India, Brazil, West Africa, and Southeast Asia, where agricultural demand for nitrogen fertilizers is high. However, the recent escalation of conflict with Israel threatens to disrupt this critical supply chain, raising concerns about global fertilizer availability and prices.

Immediate Market Reactions to the Israel-Iran Conflict

The Israeli strikes on Iran, which began early on June 13, 2025, targeted key nuclear sites, including the Natanz nuclear facility, as well as military bases and energy infrastructure vital to Iran’s economy. Iran’s retaliatory missile and drone attacks on Israel further intensified the conflict, raising fears of a broader regional war that could disrupt critical shipping lanes and energy supplies. These developments immediately impacted global commodity markets, with crude oil prices surging by 7% to $74.23 per barrel for Brent crude and $72.98 for U.S. crude on June 13. Fertilizer prices followed suit, as the Middle East’s role in both energy and fertilizer production amplified market volatility.

Industry analyses highlight the fertilizer market’s sensitivity to the conflict. For instance, while the initial Israeli strikes did not directly target fertilizer production facilities, the market reacted swiftly due to the region’s tight supply situation. Urea prices, already under pressure from reduced exports in other regions, surged as markets anticipated potential disruptions. Additionally, greater risk lies in potential disruptions to shipping lanes, particularly the Strait of Hormuz, rather than direct attacks on fertilizer plants.

Wartime Premiums and Their Impact on Fertilizer Prices

Wartime premiums—additional costs factored into commodity prices due to geopolitical risks—have become a focal point in the fertilizer market following the Israel-Iran conflict. These premiums reflect the increased uncertainty and potential for supply chain disruptions in conflict zones. In the fertilizer sector, wartime premiums are driven by several factors:

Supply Chain Vulnerabilities: The Middle East, particularly the Persian Gulf, is a critical hub for fertilizer exports. The Strait of Hormuz, through which a significant portion of global oil and fertilizer shipments pass, is at risk of closure or disruption in a wider conflict. Analysts at RBC Capital Markets warn that Iranian retaliation targeting tankers, pipelines, or energy facilities could severely impact fertilizer exports. A closure of the Strait of Hormuz could increase nitrogen and potash prices by 15–30%, according to some estimates.

Shipping and Insurance Costs: The conflict has already driven up freight rates and insurance premiums for cargo ships transiting the Persian Gulf and Red Sea. Earlier in 2025, sulfur prices from Iran surged from $130–135 per metric ton in March to $150–160 per metric ton in April due to limited port operations and higher insurance costs. Freight rates from the Middle East to Africa and Southeast Asia have risen by 25–30%, with insurance premiums doubling in some cases. These cost increases are passed on to fertilizer prices, exacerbating affordability challenges for importers.

Market Sentiment and Speculation: The fertilizer market is highly sensitive to geopolitical developments. Even without direct damage to production facilities, the mere threat of escalation has driven speculative price increases. For example, the Iranian attack on Israel earlier in 2025, while not impacting fertilizer production directly, triggered a market response that reflected the tight global supply situation. This sentiment-driven volatility has led to higher urea, anhydrous ammonia, and urea ammonium nitrate (UAN) prices.

Global Supply Constraints: The fertilizer market was already facing tight supply conditions before the Israel-Iran conflict. Reduced exports from countries like China and Russia, combined with regional production constraints in North Africa, had eliminated the global supply-demand gap. The conflict has further tightened this balance, pushing prices higher as importers scramble to secure supplies.

Regional and Global Implications

The Israel-Iran conflict’s impact on the fertilizer market extends beyond the Middle East, affecting agricultural economies worldwide. Key implications include:

Impact on Importing Countries: Countries like India, Brazil, West Africa, and Southeast Asia, which rely heavily on Middle Eastern urea exports, are adjusting their strategies to mitigate risks. India, for instance, advanced its urea tender to secure April–May cargoes in anticipation of continued instability. Importers are increasingly requesting cost and freight (CFR) contracts with flexible laycan periods or free on board (FOB) terms to manage shipping risks.

Agricultural Production Costs: Higher fertilizer prices directly increase input costs for farmers, potentially reducing crop yields or raising food prices. The Middle East’s arid climate and reliance on fertilizers for agricultural productivity make the region’s role in global food security critical. Iran and Turkey alone account for over 50% of urea consumption in the Middle East, and disruptions could exacerbate food security challenges.

Alternative Suppliers: While other Middle Eastern producers like Qatar and Saudi Arabia could partially offset disruptions in Iranian exports, their capacity to fully compensate is limited. Egypt, another regional producer, has faced its own gas supply constraints, though new gas discoveries and imports from Israel and Cyprus may bolster its production in the long term. However, these alternatives cannot immediately replace Iran’s export volume.

Geopolitical and Economic Context

The Israel-Iran conflict is rooted in decades of hostility, with Iran’s nuclear ambitions and support for proxy groups like Hezbollah and the Houthis at the core of tensions. Israel’s strikes, dubbed “Operation Rising Lion,” aimed to cripple Iran’s nuclear program and military capabilities, with Prime Minister Benjamin Netanyahu stating that the operation would continue “for as many days as it takes” to neutralize the Iranian threat. Iran’s retaliatory missile strikes, which targeted Israeli military assets but caused limited damage, underscored the risk of a prolonged conflict.

The conflict has also disrupted diplomatic efforts to address Iran’s nuclear program. Talks between the United States and Iran, scheduled to resume on June 15, 2025, in Oman, were canceled following the strikes. The United States, while denying direct involvement in Israel’s attacks, has moved military assets to the region to protect its interests and support Israel, raising the specter of a broader regional conflict.

From an economic perspective, the fertilizer market’s vulnerability to Middle Eastern instability is not new. Previous conflicts, such as the 1973 Arab oil embargo and the 1979 Islamic Revolution in Iran, led to significant energy and fertilizer price spikes. The current situation echoes these historical precedents, with analysts warning that a prolonged conflict could have a “material impact” on the global economy.

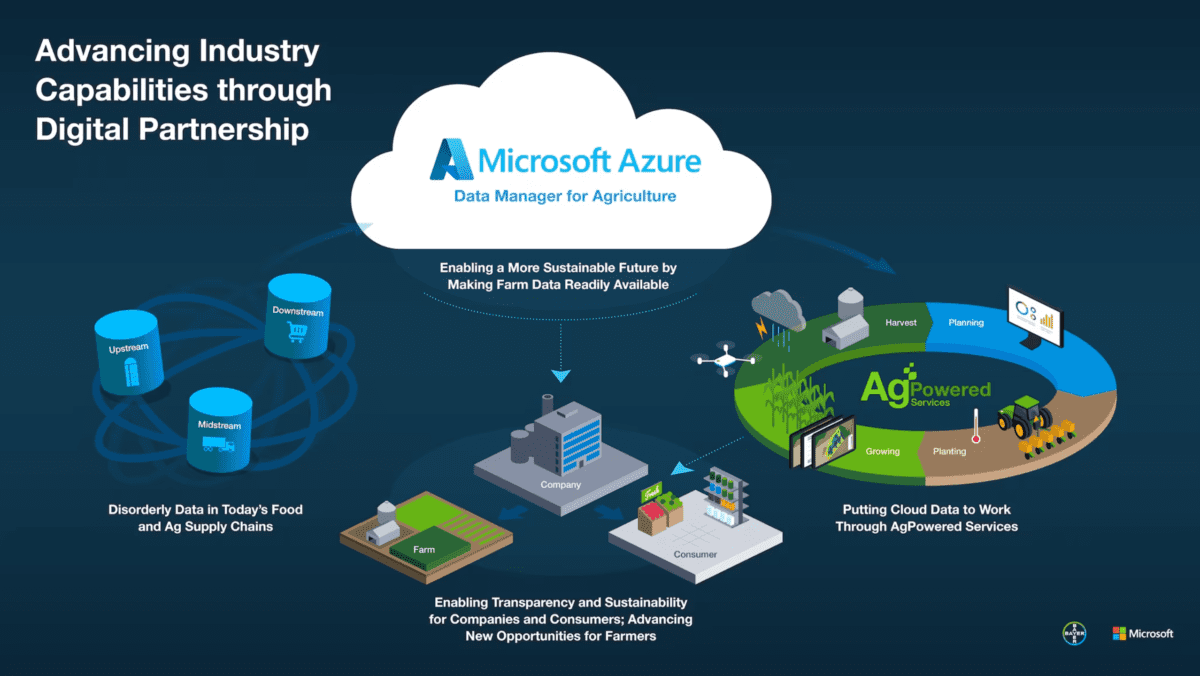

The agricultural sector is undergoing a profound transformation, driven by the convergence of geospatial data, satellite technology, and artificial intelligence (AI). Satellites silently orbiting Earth are capturing terabytes of data, while on the ground, artificial intelligence algorithms process this information to transform how we grow food. This technological marriage is reshaping not just farming practices but entire agricultural supply chains around the globe.

The Perfect Storm of Technological Convergence

Two powerful technological waves are crashing together, creating unprecedented opportunities in agriculture. In a recent AgTechTalk podcast by AgriBusiness Global, Ofer Judovits, co-founder and CEO of Marvin, explains how we’re witnessing a perfect storm of innovation, unveiled how cutting-edge technologies like geospatial data and AI are rewriting the rules of farming, carbon measurement, and supply chain logistics

The first wave comes from space. Companies like SpaceX have dramatically reduced the cost of reaching orbit, leading to a proliferation of satellites equipped with increasingly sophisticated sensors. These eyes in the sky provide high-resolution thermal imaging, soil analysis, and surface temperature readings. Even technologies like LiDAR and ground-penetrating radar—critical for regions plagued by cloud cover—are becoming more accessible and affordable.

Meanwhile, on Earth, artificial intelligence has undergone exponential growth. Advanced computer vision and deep learning models can now process the vast amounts of data streaming from space. By applying business logic to this information, AI can predict crop yields, evaluate vendor performance, assess regulatory compliance, and optimize complex supply chains.

Transforming Agriculture From Space

For farmers and agricultural businesses, these technological advancements are far from theoretical—they’re changing day-to-day operations in profound ways:

When a farmer decides where to plant, which seeds to use, or when to harvest, satellite data and AI insights now inform these critical choices. Remote sensing can detect subtle variations in soil composition, moisture levels, and plant health that would be impossible to assess manually across thousands of acres.

Financial planning has evolved from educated guesswork to data-driven forecasting. Predictive models can now estimate yields with increasing accuracy, helping businesses throughout the supply chain manage inventory, pricing, and logistics more effectively.

For crop protection and seed companies, these technologies offer a virtual experimental platform. Different treatments can be tested and monitored across diverse field conditions, accelerating R&D cycles and improving product development.

Perhaps most importantly, these technologies are revolutionizing soil health management. Satellites can monitor organic carbon content, erosion risks, and watershed conditions—essential information for sustainable agricultural practices.

Navigating Dual Challenges in the Land Sector

The broader “land sector”—encompassing agriculture, forestry, paper, timber, mining, and biofuel—faces two critical challenges that these technologies are helping to address.

First, sustainability has evolved from a marketing buzzword to a business imperative. Companies must demonstrate environmental responsibility to maintain access to global markets and command premium prices. Satellite monitoring provides transparent, verifiable data on everything from deforestation to carbon sequestration.

Second, climate change impacts—particularly disruptions to water cycles—are intensifying. In Brazil, for example, severe water scarcity in northern and central regions has pushed farmers to seek better tools for climatic risk assessment and water resource management. AI-powered predictive models can forecast drought conditions, optimize irrigation scheduling, and identify flood risks before they materialize.

Building Digital Trust Throughout the Supply Chain

Perhaps the most revolutionary aspect of this technological transformation is how it enables collaboration across entire value chains. Producers, traders, processors, manufacturers, and retailers can now exchange critical information securely.

However, this data sharing requires new models of digital trust. Drawing lessons from cybersecurity, agricultural technology companies are developing frameworks that support information exchange while preserving data privacy and ownership. This balance is crucial for creating transparent supply chains without compromising competitive advantages or sensitive information.

As these technologies continue to evolve, they promise not just incremental improvements but a fundamental reimagining of how we grow food, manage natural resources, and build resilient agricultural systems capable of feeding a growing global population in an increasingly unpredictable climate.

Scientists at MIT have developed a new breed of robotic insects – lighter than a paperclip – capable of sustained flight and impressive aerial acrobatics. These miniature marvels could revolutionize indoor farming, a burgeoning sector crucial for addressing global food security challenges.

“These robots could unlock a whole new realm of possibilities,” explains Suhan Kim, co-lead author of the study. “Imagine precisely guiding these tiny machines to pollinate delicate blossoms within a controlled environment. This technology could significantly boost yields in vertical farms, where honeybee presence might not always be feasible.”

Vertical farming, with its multi-tiered growing systems, offers a promising solution to the growing demands of a burgeoning population. However, traditional pollination methods can be challenging in these controlled environments. Enter the robo-insect – a potential game-changer for sustainable agriculture.

“Our goal isn’t to replace honeybees entirely,” emphasizes Kim. “However, in indoor settings where honeybee colonies might not be viable, these robots could offer a valuable alternative.”

While still under development, these miniature marvels are constantly evolving. Researchers are focused on enhancing flight time and precision, aiming for pinpoint landings on the heart of each flower.

This cutting-edge research published in the journal Science Robotics, represents a significant step towards a future where technology seamlessly integrates with nature, fostering a more sustainable and resilient food system.

The World Economic Forum’s (WEF) Future of Jobs Report, a bi-annual study, has become a key resource for understanding the evolving global labor market. The 2025 edition offers a detailed look at the trends and challenges that will shape the next five years, drawing on a survey of over 1,000 employers representing more than 14 million workers across 55 economies and 22 industry clusters. This year’s report emphasizes the interconnectedness of various factors, from technological advancements to economic and geopolitical shifts, and their combined impact on the job landscape.

Key Macrotrends Reshaping the Labor Market

The report identifies five major macrotrends that are significantly impacting the labor market:

Technological Change: This includes the expansion of digital access, advancements in artificial intelligence (AI) and information processing, and increased use of robotics and automation. Broadening digital access is seen as the most transformative trend, with 60% of employers expecting it to significantly change their businesses by 2030.

The Green Transition: Increased efforts to reduce carbon emissions and adapt to climate change are driving changes across industries.

Geoeconomic Fragmentation: Geopolitical tensions and increased restrictions on trade and investment are impacting business models.

Economic Uncertainty: The rising cost of living and slower economic growth are creating significant challenges for employers and workers.

Demographic Shifts: Aging populations and variations in working-age populations are also impacting labor markets.

Impact on Jobs: Growth and Decline

The interplay of these macrotrends is expected to result in a “structural labor market churn” of 22% of jobs, with 170 million new jobs created and 92 million displaced by 2030. While this represents a net increase of 78 million jobs, the changes will not be evenly distributed. Technological change is predicted to be the most divergent force, both creating and displacing jobs.

Skills in Demand to Adapt to a Changing Landscape

The skills required by workers are also evolving rapidly. The report highlights the following as key skills for the future:

Analytical thinking remains a core skill for employers.

Resilience, flexibility, and agility are seen as essential.

Technological literacy, AI and big data, and networks and cybersecurity are among the fastest-growing skills.

Creative thinking, and curiosity and lifelong learning are also gaining in importance.

Human-centered skills are still crucial, as many jobs require complex problem-solving, nuanced understanding and sensory processing that are difficult for AI to replicate.

A Closer Look at the Agricultural Sector

The agriculture, forestry, and fishing industry faces a unique set of challenges and opportunities within this changing landscape. The sector is heavily influenced by:

Climate change and the need for climate mitigation and adaptation.

The rising cost of living.

While important, digitalization is less of a driver in agriculture than in other sectors. For example, only 70% of employers in the agricultural sector expect an increase in AI and big data use.

Despite the slow adoption of some advanced technologies, the agriculture sector is expected to see significant job growth, with farmworkers predicted to see the largest absolute growth of any job type, an estimated 35 million new jobs by 2030. This growth is driven by the green transition, broadening digital access, and rising costs.

Skills gaps are a primary barrier to transformation for this industry, as is an outdated regulatory framework. The sector also faces challenges in attracting new talent, and needs to address insufficient data infrastructure.

The report also highlights regional variations, as the impact of these trends will vary by geography. For example:

Companies in Eastern Asia and Oceania anticipate labor market transformations due to aging and declining working-age populations, and slower economic growth.

Navigating the Future of Work

The Future of Jobs Report 2025 emphasizes the need for proactive and collaborative efforts to navigate the complexities of the evolving labor market. It is critical for businesses, governments, and workers to:

Focus on skills development and continuous learning.

Embrace technological advancements and their potential to augment human capabilities.

Adopt more flexible hiring practices to address shortages.

Improve diversity, equity, and inclusion to broaden the talent pool.

Support employee health and well-being.

Invest in infrastructure.

Adapt to a more dynamic, and fluid global economy.

Initiatives like the Reskilling Revolution and the Jobs Initiative are aimed at creating a more inclusive and future-ready workforce. The choices made today will determine the future of work and the opportunities it provides for everyone.

In an increasingly uncertain world, where the demand for food is skyrocketing and the pressures on our environment are mounting, the question looms large: how will we sustainably feed a global population that could reach 9.6 billion by 2050? The 2024 Global Agricultural Productivity (GAP) Report sheds light on this challenge, calling for a shift in how we grow food and manage our land. At the heart of the issue lies the need to boost total factor productivity (TFP)—the efficiency with which we turn agricultural inputs into food. But the reality is stark: TFP growth, which averaged just 0.7% annually from 2013 to 2022, falls well short of the 2% needed to meet future demand.

Why TFP Matters

What’s at stake? Without TFP growth, we face a future where we either run out of resources or destroy the very environment we depend on. Total factor productivity isn’t about just growing more food—it’s about doing so smarter, using fewer resources like land, water, and fertilizers. It’s about protecting the environment while ensuring farmers can make a living, and consumers can afford healthy, nutritious food.

The “Valley of Death” in Agriculture

We live in a world brimming with innovation. New technologies are constantly being developed to improve farming—from advanced machinery to precision agriculture. Yet, many of these innovations remain stuck on the shelf, unable to reach the farmers who need them most. This gap between innovation and adoption—what experts call the “valley of death”—is one of the biggest obstacles to productivity growth. Why does this happen? Smallholder farmers, who produce much of the world’s food, often lack access to the tools, knowledge, and financing necessary to make these technologies work for them.

Bundling Solutions: A New Approach

The GAP Report proposes a new way forward: combining proven agricultural practices with emerging technologies in “bundles” that are tailored to local needs. By integrating new tools with effective distribution systems and supportive policies, we can help farmers overcome the barriers that prevent them from embracing change. It’s about creating practical solutions that fit the realities of their lives—solutions that make farming more productive and sustainable without overwhelming them with complexity.

A Success Story from South Asia

South Asia offers a hopeful example of what’s possible. Over the past decade, the region has been a standout performer in terms of agricultural productivity. Thanks to smart investments in research, mechanization, and digital innovations, South Asia’s TFP growth has outpaced much of the world, averaging 1.44% annually from 2013 to 2022. This success wasn’t a fluke—it was the result of deliberate, sustained efforts to modernize agriculture and bring farmers the tools they need to thrive. If South Asia can lead the way, why not other regions?

The Path Forward: What Needs to Change

To get the world’s agricultural productivity back on track, we need to focus on five key areas:

Investing in Innovation: The gap between what farmers need and what’s available in terms of technology and know-how is still far too wide, especially in low- and middle-income countries. We must close this gap by investing in agricultural research and development (R&D) and making sure innovations reach the people who need them most.

Opening Up Markets: Access to markets is critical for farmers to sell their products at fair prices and purchase the inputs they need to increase productivity. Strengthening market infrastructure—both physical and digital—can create more opportunities for farmers to thrive.

Fostering Trade: International trade can help farmers by creating larger markets for their products and facilitating the exchange of knowledge and technology. However, trade barriers—especially in developing regions—must be addressed to unlock the full potential of global agricultural productivity.

Cutting Food Waste: We waste far too much of what we produce. Reducing food loss and waste, particularly in the supply chain, can increase the amount of usable food and reduce the strain on natural resources.

Building Partnerships: No one can solve these challenges alone. Governments, businesses, researchers, and local communities must come together to create sustainable solutions. Public-private partnerships can help scale the innovations that will drive the next wave of agricultural productivity growth.

Conclusion: A Call to Action

The world’s farmers face enormous challenges, but they also hold the key to a more sustainable, food-secure future. By adopting new technologies, improving access to markets, and working together across sectors, we can power the productivity gains needed to feed the world’s growing population. The 2024 GAP Report reminds us that while the road ahead is difficult, it is not impossible. With the right investments and policies, we can build a future where both people and the planet thrive.

This is not just a call for action from governments and industries; it’s a call for each of us to recognize the importance of sustainable agriculture. By supporting these efforts, we contribute to a future where farmers have the tools they need to nourish the world, sustainably.

✍️ A bill designed to nurture and grow the mung bean industry in Kenya was rejected by the National Assembly this week.

The Mung Beans Bill, 2022, is a proposed Kenyan law designed to establish a regulatory framework for the mung bean sector’s growth. The bill’s objectives include outlining responsibilities for both national and county governments, such as setting quality standards, providing technical assistance, facilitating market access, and encouraging the use of mung beans in government feeding programs. It also proposes a licensing system for mung bean marketers, processors, and traders.

The National Assembly, however, rejected the bill at the second reading stage. Initially sponsored by Senator Enoch Wambua in the Senate and co-sponsored by Hon. Paul Nzengu in the National Assembly, the bill was published on December 30, 2022, and read for the first time in the Senate on February 15, 2023. It was then passed by the Senate and referred to the National Assembly for approval.

The rejection by the National Assembly means that the bill will now be sent to a mediation committee. The Speakers of both the National Assembly and Senate will appoint an equal number of members to form the mediation committee to consider an agreed version of the bill. The committee has 30 days to develop a mediated version. Once completed, the committee will present a report with the mediated version to both Houses. If both Houses approve it, the bill will be considered passed.

The Mung Beans Bill aimed to modernize mung bean farming techniques and improve the sector’s productivity while integrating the crop into government programs, but the current rejection indicates that further negotiation is needed to find a mutually acceptable version of the bill for both legislative bodies.

As we approach the end of 2024, the agroindustry continues to grapple with a complex interplay of global events. The “Black Swans” predicted at the outset of the year have indeed materialized, shaping the industry’s trajectory in unexpected ways. Let’s delve into the key developments and explore strategies for navigating this challenging landscape.

Black Swan 1: A Shifting Economic Paradigm

The initial prediction of agroindustry stagflation has evolved into a more nuanced reality. While inflation has been somewhat tempered, the sector is experiencing a delicate balance between price stability and economic stagnation. The decline in input costs, particularly for fertilizers, offers some respite. However, the recent surge in fuel prices due to production cuts by OPEC+ nations adds renewed pressure.

The global economic outlook remains uncertain. The International Monetary Fund (IMF) in its July 2024 World Economic Outlook update projected global growth to slow from an estimated 3.5 percent in 2023 to 3.0 percent in 2024 and 2025. The looming possibility of increased taxes in the United States, coupled with the ongoing impact of high national debt and rising interest rates in major economies, creates a challenging environment for businesses seeking to expand or innovate.

Black Swan 2: The Enduring Challenge of China

The Chinese agrochemical industry’s overcapacity continues to exert significant pressure on the global market. Despite efforts to address this issue, the oversupply of inexpensive products has eroded margins for many manufacturers. This trend is likely to persist, necessitating strategic adjustments by industry players.

Black Swan 3: Energy Dynamics

The energy landscape has been marked by volatility. While there was an initial oversupply leading to lower prices, recent production cuts by OPEC+ have driven a surge in fuel costs. This impacts the profitability of energy producers and increases costs across the supply chain, including agriculture. The ongoing search for new energy markets and the potential for geopolitical disruptions remain significant uncertainties.

Black Swan 4: Geopolitical Tensions

The global political landscape remains tense. The ongoing conflict in Ukraine continues to disrupt supply chains and impact market confidence. Additionally, escalating tensions in the Middle East and Northeast Asia add to the uncertainty. These conflicts, coupled with the lingering effects of trade wars, create a volatile environment that can disrupt supply chains and impact market confidence.

Black Swan 5: Interest Rate Volatility

Central banks around the world are grappling with inflation and economic uncertainty. The U.S. Federal Reserve has indicated a potential for further interest rate hikes in 2024, which could have a ripple effect on global markets. This, coupled with the potential for increased taxes in the U.S., could further strain businesses and exacerbate the challenges posed by high-interest rates.

Beyond the Five Swans

While the five primary Black Swans have dominated the narrative, other factors, such as labor shortages, climate change-induced extreme weather events, evolving regulatory pressures, and rapid technological advancements, have also played a significant role in shaping the agroindustry. These trends are likely to persist and will require ongoing adaptation.

Preparing for the Future

Navigating this complex landscape requires a proactive approach. Businesses should prioritize the following strategies:

Cost Control: Implement rigorous cost-cutting measures to maintain profitability in a challenging economic environment. Explore energy-efficient practices and consider alternative energy sources to mitigate rising fuel costs.

Strategic Investments: Identify growth opportunities and make strategic investments to expand market share and enhance competitiveness. This might include investing in R&D for climate-resilient crops or precision agriculture technologies.

Cash Flow Management: Maintain a strong cash position to weather economic downturns and seize opportunities when they arise.

Adaptability: Embrace flexibility and innovation to respond to changing market conditions and emerging challenges. Stay informed about geopolitical developments and adjust supply chain strategies accordingly.

Sustainability: Integrate sustainable practices into your operations to address climate concerns and meet evolving consumer demands.

The agroindustry in 2024 has been characterized by a confluence of global challenges. While the initial predictions have largely materialized, the evolving nature of these events requires ongoing assessment and adaptation. By understanding the key trends and implementing effective strategies, businesses can navigate this complex landscape and position themselves for long-term success.

Disclaimer: The information provided in this article is based on the current understanding of global events as of September 2024. The situation is dynamic and subject to change.

Kenya’s vast Arid and Semi-Arid Lands (ASALs) encompass a staggering 80% of the country’s landmass. This region, home to roughly 16 million Kenyans, is a land of stark beauty and harsh realities. Pastoral communities have carved out a life here for generations, their existence intricately linked to the health of their livestock. These regions, though crucial for Kenya’s beef industry, grapple with food insecurity due to unpredictable rainfall, economic hardships, and even conflict.

Despite these challenges, the potential for a thriving beef sector in ASALs remains. Beef cattle make up a significant portion of Kenya’s national herd, with nearly half originating from these very regions. However, there’s a disconnect between this potential and the reality of poverty faced by ASAL communities.

In spite of their ingenuity and deep understanding of this unforgiving environment, ASAL residents grapple with some of the nation’s highest poverty rates. The land itself presents a multitude of challenges. Rainfall is erratic and scarce, punctuated by devastating droughts. This unpredictability makes crop cultivation a gamble, and forces pastoralists to constantly be on the move, seeking grazing pastures for their herds.

Limited access to finances, infrastructure issues like poor roads, and the harsh environment itself all contribute to this disparity. Traditional pastoral practices lack formal financial inclusion, hindering investments in better grazing lands, veterinary care, and essential supplies. Additionally, the unpredictable nature of droughts constantly threatens livelihoods.

These challenges are further compounded by a lack of infrastructure. Remote locations make it difficult for farmers to get their cattle to market, limiting profit margins and hindering investment in their herds. The absence of reliable financial systems also restricts access to loans and insurance, crucial tools for weathering the inevitable storms, both literal and metaphorical.

The consequences of these hardships are stark. Food insecurity is a constant threat, malnutrition rates are high, and disease outbreaks can decimate herds, plunging families deeper into poverty. Conflict, often sparked by competition for scarce resources, adds another layer of complexity to this already precarious situation.

However, amidst these struggles, there are glimmers of hope. The Kenyan government recognizes the critical role that a thriving ASAL region plays in the nation’s economic well-being. Beef production is a cornerstone of the ASAL economy, with these regions contributing nearly half of Kenya’s national herd.

There’s immense potential for growth, but unlocking it requires a multi-pronged approach. Strengthening market access is crucial. Reliable transportation networks and improved marketing infrastructure are essential for connecting farmers to lucrative markets and ensuring they receive fair prices for their cattle.

Cooperatives offer a promising pathway towards a more secure future for ASAL communities. By pooling resources, farmers gain greater bargaining power, access to better deals, and opportunities for value addition. This collaborative approach can empower them to become more resilient in the face of climate shocks and economic downturns.

Investing in education and promoting financial inclusion are equally important. Equipping communities with the knowledge and tools to manage their herds more effectively and navigate financial systems can go a long way in building a more secure future for the people living in the ASALs.

FAO Report Indicates the Devastating Effects of Disasters on Agriculture

The world is facing a new normal: a relentless barrage of disasters hammering agricultural systems. From the devastating swarms of desert locusts in East Africa to the relentless hurricanes in the Atlantic, these events leave a trail of destruction, impacting not just farmers’ livelihoods but also our global food security.

This article, based on a report by the Food and Agriculture Organization (FAO), dives into the economic and nutritional consequences of disasters on agriculture, explores the most impactful disaster types, and emphasizes the urgent need for building resilient agricultural systems.

The Economic Toll of Disasters

Disasters inflict a heavy economic blow on agriculture, the sector most vulnerable to their wrath. Lower crop and livestock production translate to billions of dollars in losses.

Between 2008-2018, disasters caused staggering losses:

USD 30 billion in sub-Saharan Africa and North Africa

USD 29 billion in Latin America and the Caribbean

USD 8.7 billion across Small Island Developing States (SIDS) in the Caribbean

USD 49 billion in Asia

Disaster Hall of Shame: The Top Culprits

While all disasters wreak havoc, some stand out for their devastating impact on agricultural production in least developed countries (LDCs) and low to middle income countries (LMICs) from 2008-2018:

Drought: The undisputed champion of agricultural devastation, responsible for over 34% of crop and livestock production loss (USD 37 billion).

Floods: The runner-up, causing USD 21 billion in losses (19% of the total).

Storms: Particularly destructive in 2017, responsible for USD 19 billion in losses (18% of the total).

Pests, Diseases & Infestations: Biological threats like the 2020 desert locust crisis contribute 9% to production loss.

Wildfires: Though seemingly less impactful (USD 1 billion in losses), wildfires can have devastating consequences on forestry and ecosystems.

Disasters and Nutrition

The impact of disasters extends far beyond economic losses. Reduced agricultural production translates to significant nutritional deficiencies. Between 2008-2018, disaster-induced production losses resulted in:

Africa: Potential loss of 559 calories per capita per day (20% of Recommended Daily Allowance – RDA)

Latin America & the Caribbean: Potential loss of 975 calories per capita per day (40% of RDA)

Asia: Potential loss of 283 calories per capita per day (11% of RDA)

Building Resilience

The time for action is now. We must transform how we manage disasters to safeguard our food security. Effective national strategies on disaster risk reduction (DRR) require a comprehensive understanding of disaster impacts on agriculture, including:

Identifying damage and loss patterns across crops, livestock, forestry, fisheries, and aquaculture.

Building profiles of all types of disasters, from rapid-onset catastrophes to slow-moving droughts and localized events.

Expanding disaster assessments to consider pandemics, food chain crises, conflicts, and protracted crises.

Integrating disaster risk reduction with climate change adaptation strategies.

For a Deeper Dive:

The full FAO report, “The impact of disasters and crises on agriculture and food security 2021,” offers a wealth of information on disaster impacts and practical recommendations for building resilient agricultural systems. By understanding the challenges and implementing effective solutions, we can create a future where agriculture can weather any storm and nourish a food-secure world.

Kenya’s newest champion is a delicious creamy fruit: the avocado, which is rapidly climbing the export charts, making Kenya the undisputed avocado king of Africa, and a strong contender globally.

Europe’s already a fan, and Kenya’s setting its sights on massive markets like India and China. While Mexico remains the undisputed leader, Kenya’s exports skyrocketed by a whopping 24% last year – the highest growth among major producers.

Kenya’s got a natural advantage. Perfect growing conditions exist between 1,500 and 2,100 meters above sea level, and luckily, that’s where much of the Kenyan landscape sits. Sustainability is another win. Abundant rainfall in the highlands means most farms don’t need extra water, except during the dry season. Even then, water usage is incredibly efficient, with some farms using less than 100 liters per kilogram of avocado – way below the global average. Plus, year-round equatorial sunshine allows the avocados to “grow by day and sleep at night,” as one industry insider playfully puts it.

Kenya also has a lucky harvest window. Their avocados hit the market before many competitors’, giving them a head start. Some regions even enjoy double harvests thanks to two rainy seasons, extending their selling period. Savvy small-scale farmers are jumping on board too, as well-maintained avocado trees start producing decent yields within a few years.

Labor costs are another factor in Kenya’s favor. While wages are lower than some competitors, some larger Kenyan growers offer above-average pay. And for consumers, the price difference is stark. A ripe avocado in a Kenyan market can be found for mere pennies, while a single fruit in European supermarkets might cost several dollars, depending on the season.

Demand is on the rise too. While the US devours a massive chunk of global imports, Europe’s love affair with the avocado is blossoming as well. Last year, Germans and Poles saw their avocado consumption increase by 10% and 24% respectively.

It’s not all sunshine and rainbows though. Maintaining high standards for quality, traceability, and sustainability is crucial, as every exported avocado represents Kenya’s reputation. In the past, there have been concerns about unripe avocados reaching the market. The agricultural authorities even intervened last year to prevent exports from some smallholders who lacked proper storage and irrigation techniques.

Shipping also presents challenges. Precise temperature control is essential, and with the Red Sea currently unavailable due to regional conflicts, the longer route around South Africa adds both cost and risk of spoilage.

Despite these hurdles, Kenya is not only a leader in renewable energy, but also a champion of a different kind of green economy – one fueled by delicious avocados.

The humble potato has avoided a major identity crisis! The U.S. Dietary Advisory Committee (DAC) recently confirmed that potatoes will remain classified as a vegetable, settling a debate that had simmered within the committee during its work on the 2025 Dietary Guidelines for Americans.

In 2023, as the DAC embarked on revisions to the dietary guidelines, the possibility of reclassifying potatoes as a grain alongside rice and corn was raised. This consideration stemmed from the potato’s starch content, a characteristic it shares with grains. However, this reclassification sparked concerns

Opponents of the reclassification, including US Senator Susan Collins, highlighted the potato’s well-rounded nutrient profile. Unlike many grains, potatoes boast a good amount of vitamins C and B6, alongside potassium and protein – nutrients more commonly associated with vegetables like kale, spinach, and broccoli. Studies like one published in the “NIH National Library of Medicine” have shown that potatoes can be a valuable source of these essential vitamins and minerals, especially when consumed with the skin.

Senator Collins emphasized the potential public health implications of the shift. “Reclassifying potatoes as grains,” she stated, “would have sent a false message… that potatoes are not healthy.” This concern aligns with research from Harvard University which suggests that consumers tend to make dietary choices based on food category labels. A shift to the “grains” category could have discouraged people from consuming potatoes, a potentially negative outcome considering their affordability, long shelf life, and versatility in recipes.

The decision to retain the potato’s vegetable status has been welcomed by the potato industry. Bob Mattive, president of the National Potato Council, called it a “positive development,” underscoring the importance of recognizing the potato’s unique nutritional profile within the vegetable category.

This episode highlights the ongoing discussions surrounding food categorization and its impact on dietary choices. As we strive for clearer and more informative dietary guidelines, the importance of considering a food’s complete nutritional profile alongside its individual components becomes even more evident.

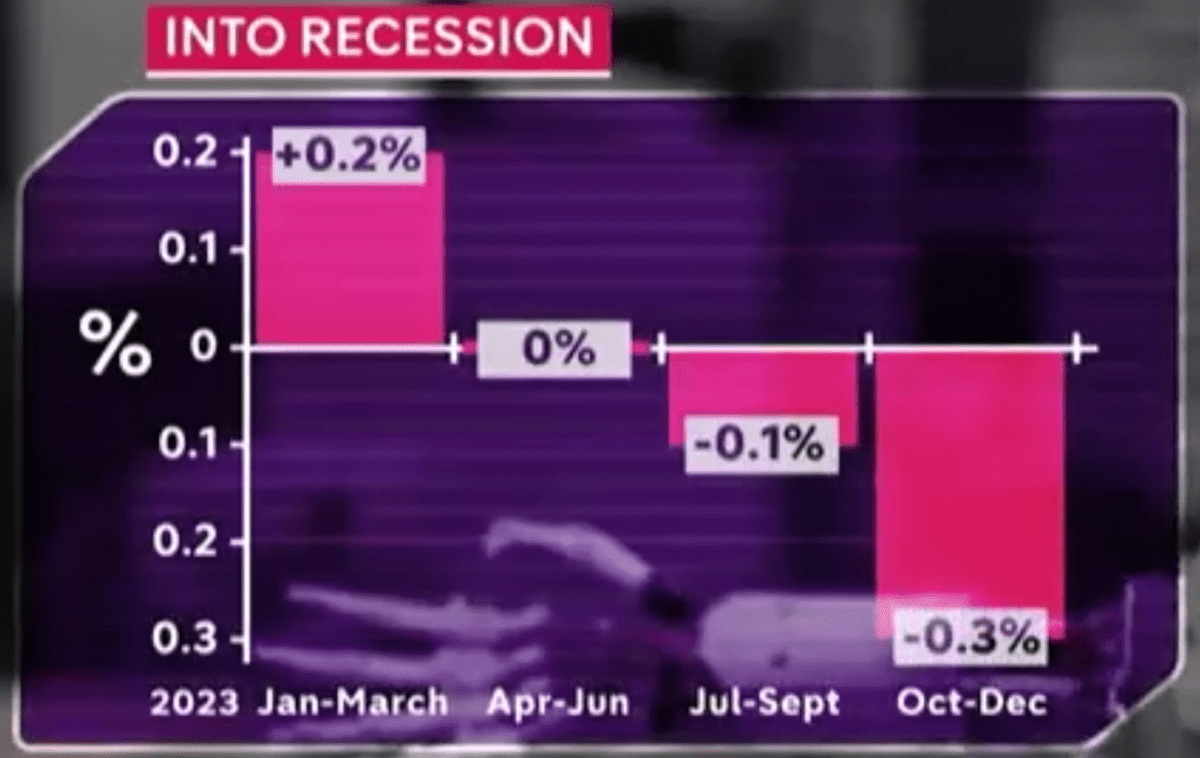

The UK economy officially entered a recession in the second half of 2023, as defined by two consecutive quarters of negative GDP growth. The final quarter of 2023 saw a contraction of 0.3%, exceeding most predictions. Several factors contributed to the recession, including (1) high inflation caused by rising energy and food prices, which have placed immense pressure on households and businesses; (2) interest rate hikes as a consequence of the actions of the Bank of England to combat inflation, but this also dampened economic activity; and (3) a global economic slowdown, further impacting the UK’s export-oriented sectors.

The recession is already having a noticeable impact on the UK, with job losses as businesses are cutting costs and hiring freezes becoming more common. There is also reduced consumer spending due to rising costs and economic uncertainty, as well as lower living standards since many people are struggling to afford basic necessities due to inflation.

With the winds of change blowing across the global economy, many in the agricultural sector, particularly in Africa, are understandably concerned. While the UK’s economic woes might seem distant, the interconnectedness of our world means the ripples will be felt far and wide. This is because the UK is a major buyer of Africa’s horticultural products, tea, coffee, among others. Reduced demand for exports, potential trade disruptions, and tighter investment belts—these are just some of the challenges African agriculture might face.

Will farmers’ hard work, sweat, and hope be swept away in this economic storm?

Imagine the sting of sunburnt shoulders after a long day on the farm. The calloused hands, the grit on a farmer’s boots, the quiet satisfaction of watching life burst from the earth! That’s the heartbeat of African agriculture, a rhythm that’s about so much more than just crops. It’s about families, communities, and the very foundation of life on this continent.

The UK might be tightening its belt, but the world is a vast and hungry place. For Africa, it’s time to explore new trade routes and chart new courses. Here’s the thing: Africa has weathered storms before, and it’ll weather this one too. For Africa, this is not a time for despair, but for strategic thinking and proactive measures that turn challenges into opportunities. The continent majorly relies on farmers, after all, and adaptability is in their blood—farming is their business!

It’s important to note that the exact impact of the UK recession on global markets and African agriculture is difficult to predict, as it depends on several factors like the severity and duration of the recession, government interventions, and global economic trends. It is important to note that the severity and duration of the UK recession are still unclear. Some economists believe it will be short-lived, while others predict a more prolonged downturn. The UK government is already implementing various measures to mitigate the impact, but the ultimate outcome will depend on a complex interplay of domestic and global factors.

Turning challenges into opportunities

The impact of the UK’s recession might be unevenly distributed across different regions and sectors in Africa, and some African countries might even benefit from opportunities arising from the changing global economic landscape. The UK recession might cast a shadow, but for African agriculture, it can also be an opportunity to reimagine, reshape, and emerge stronger. By working together, embracing innovation, and fostering resilience, African countries can navigate these uncertain waters and achieve economic gains. This can only happen by being nimble and embracing new technologies, digging into data-driven solutions, and finding smarter ways to farm. Who knows, maybe Africa will even discover a hidden gem that will become the next revolutionary agricultural technique!

In order to thrive, Africa must chin up and face the future with the same determination that pushes its farmers out into the fields each morning, the same hope that sees a tiny seed transform into a life-giving fruit.

As the global population continues to expand, so does the demand for food. Agriculture, the backbone of sustenance, faces a daunting challenge: how to feed an ever-growing population with limited resources and a shrinking agricultural workforce. The recent findings from the 2022 Census of Agriculture conducted by the United States Department of Agriculture (USDA) shed light on a concerning trend that has significant implications not only for the United States but also for agricultural systems worldwide.

According to the census, the number of farms in the United States has declined steadily over the past two decades. In 2022, there were 1,900,487 farms, a decrease from 2,042,220 farms in 2017. This decline, totaling 141,733 farms, reflects a broader trend of consolidation and restructuring within the agricultural sector. Family-owned farms, which comprise 95 percent of the total, have been particularly affected, signaling a shift in the demographic composition of agricultural producers.

Even more alarming, the amount of land dedicated to farming has also decreased. Despite the vast expanse of agricultural land in the United States, farmers are now working on 20,116,728 fewer acres compared to 2017. This reduction, equivalent to the size of South Carolina, shows the intensifying pressure on available arable land. The average size of farms has increased slightly, indicating a consolidation of land holdings among fewer producers.

The implications of these trends extend beyond the borders of the United States. With a growing global population projected to reach 9.7 billion by 2050, the world faces an unprecedented demand for food. Agriculture must not only meet this demand but also adapt to evolving environmental challenges, such as climate change and land degradation. The decline in the agricultural workforce exacerbates these challenges, as fewer farmers are tasked with producing more food to feed a burgeoning population.

The study by USDA has also shown that the digital divide persists within the agricultural sector, with only 79 percent of U.S. farms having internet access. While advancements in technology have the potential to increase efficiency and productivity, access to these innovations remains unequal, further widening the gap between large-scale commercial farms and smaller, resource-constrained operations.

In the face of these developments, policymakers, agricultural stakeholders, and international organizations must prioritize strategies to bolster the agricultural workforce and promote sustainable farming practices. This includes investing in education and training programs to attract and retain a new generation of farmers, enhancing access to land and resources for smallholders, and leveraging innovations and technology to improve productivity and resilience.

In the hustle and bustle of daily life, caffeine serves as the universal catalyst that jump-starts our mornings, with coffee being the preferred vessel for this beloved stimulant. Cultivated across more than 70 nations, coffee holds a prominent place in our lives, supporting the livelihoods of approximately 125 million people globally. However, the warming climate threatens this vital commodity, prompting the need for innovative solutions to safeguard our morning cup of coffee.

As reported by “THE Economist,” the escalating temperatures and shifting rainfall patterns in key coffee-producing regions of South America, central Africa, and South-East Asia pose a significant threat to the industry. According to a recent study by Cássia Gabriele Dias from the Federal University of Itajubá in Brazil, between 35% and 75% of Brazil’s coffee-growing land may become unusable by the end of the century.

Acknowledging the severity of this issue, the global coffee community is now faced with the challenge of implementing Climate-Smart Policies and Investments to ensure the industry’s sustainability. Drawing from our extensive review of previous global changes in the coffee industry, we delve into creative approaches that can transform the coffee landscape.

Climate-Smart Solutions for Coffee Farms

One intriguing option is to shift coffee cultivation uphill, capitalizing on the natural temperature decrease with altitude. Tanzania, for instance, boasts areas 150 to 200 meters above current coffee-growing zones, presenting an opportunity for continued coffee farming. However, this approach introduces challenges such as steeper slopes, shallower soils, and potential conflicts with climate pledges.

An alternative strategy involves revisiting traditional “agroforestry” techniques, as highlighted by Nicholas Girkin, an environmental scientist at the University of Nottingham. Historically, coffee plants thrived in the shade beneath taller trees, offering protection against scorching temperatures. Recent studies indicate that these agroforestry practices not only enhance the flavor and size of coffee beans but also promote biodiversity, with trees acting as havens for beneficial predators and pollinators.

While agroforestry presents a viable short-term solution, it has its limitations. Climate models project that in many regions, temperatures may eventually surpass the tolerance levels of the sensitive Arabica plant. This necessitates a more profound transformation in the coffee industry—a change in the very nature of the coffee bean itself.

Rediscovering Forgotten Gems: Diverse Coffee Species for a Changing Climate

In the pursuit of a resilient coffee plant, scientists are revisiting overlooked coffee species that flourished in warmer or drier environments. Botanist Aaron Davis, from the Royal Botanic Gardens, Kew, has dedicated his efforts to exploring forgotten varieties such as Coffea stenophylla and Coffea affinis. These species, found in Sierra Leone, exhibit promising traits, hinting at their ability to withstand higher temperatures compared to Arabica and Robusta.

Research indicates that C. stenophylla boasts a fruitier profile and better acidity than Brazilian Arabica, offering a potential replacement for the vulnerable species. Additionally, Coffea dewevrei, known as Excelsa, emerges as an attractive option due to its heat tolerance, high yield, and resistance to the coffee-rust fungus.

Genetic Engineering and Cross-Breeding

Recognizing the urgency of the situation, researchers are exploring a combination of genetic engineering and cross-breeding to transfer desirable traits from these resilient species into Arabica. Dr. Davis, involved in comprehensive Arabica genome research, aims to facilitate this transformative process. However, the timeline for commercial use of a new coffee cultivar remains a decade or more.

In the interim, agricultural engineer Dr. Dias emphasizes the need for immediate measures, urging coffee-producing nations like Brazil to adopt a dual strategy—moving some farms uphill while incorporating agroforestry practices. This strategic approach can provide a temporary buffer, allowing scientists the time required to develop a coffee plant capable of thriving in a warmer world.

In summary, the future of our morning cup of coffee lies in the hands of innovative solutions, blending traditional wisdom with cutting-edge technology. As we navigate the challenges posed by climate change, the global coffee community must unite in its commitment to sustainable practices, ensuring the longevity of this cherished beverage.

In the midst of a global technological revolution, the potential for artificial intelligence (AI) to reshape economies is both thrilling and concerning. As we navigate the complexities of AI, it becomes imperative to explore how this transformative technology can revolutionize the agricultural sector, particularly in the context of Africa.

The Impact of AI on Global Labor Markets

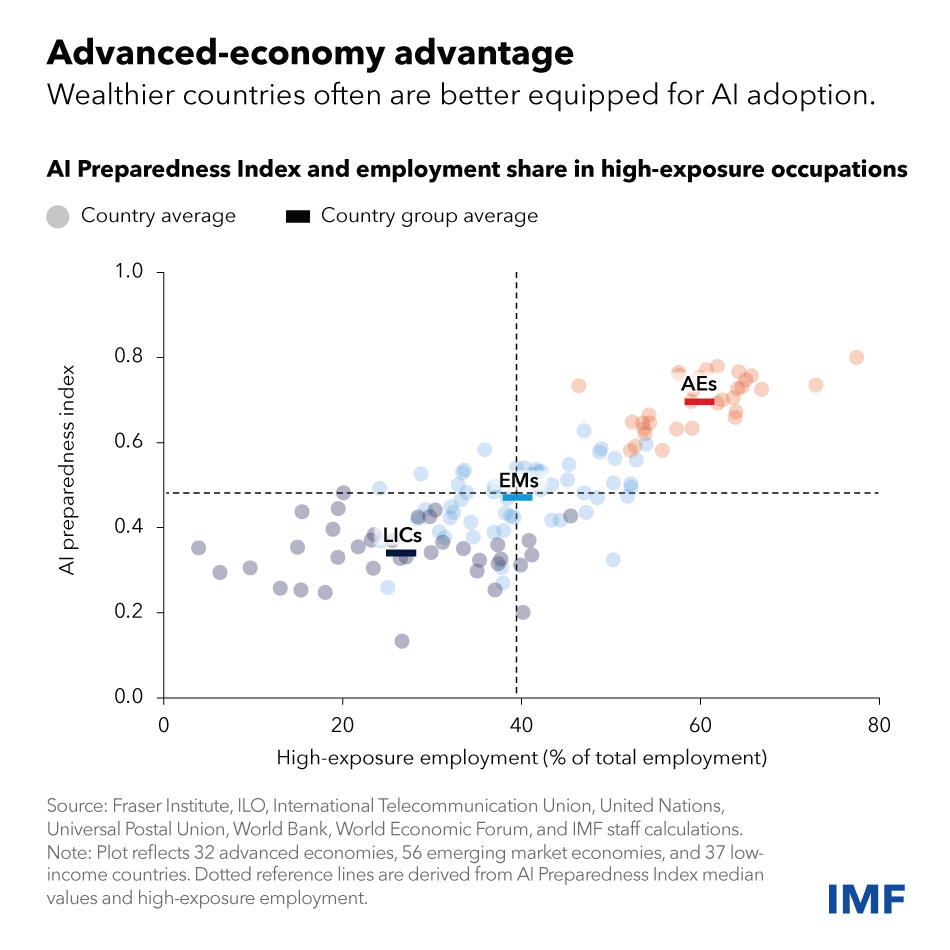

Before delving into the specifics of agriculture, it is crucial to understand the broader implications of artificial intelligence on the global economy. According to recent analysis by the International Monetary Fund (IMF), nearly 40 percent of global employment is exposed to artificial intelligence. Unlike previous technological advancements, AI has the unique capability to impact highly skilled jobs, creating both risks and opportunities.

In advanced economies, where approximately 60 percent of jobs may be affected by artificial intelligence, there is a dual prospect of job enhancement and displacement. Meanwhile, emerging markets and low-income countries face a lower immediate disruption rate of 40 percent and 26 percent, respectively. However, the lack of infrastructure and skilled workforces in these regions poses a risk of exacerbating global inequality over time.

AI’s Influence on Inequality and the Labor Market

The IMF’s findings also suggest that artificial intelligence could exacerbate income and wealth inequality within countries. As AI becomes integrated into businesses worldwide, there is a potential for polarization within income brackets. Workers adept at harnessing artificial intelligence may experience increased productivity and wages, while those unable to adapt could fall behind.

To mitigate this risk, policymakers are urged to establish comprehensive social safety nets and retraining programs for vulnerable workers. The goal is to ensure an inclusive transition to an AI-driven world, protecting livelihoods and curbing inequality.

AI Preparedness Index: Crafting Inclusive Policies

The AI Preparedness Index, measuring readiness in key areas such as digital infrastructure, human capital, innovation, and regulation shows that wealthier economies, including advanced and some emerging market economies, tend to be better equipped for AI adoption. However, there is considerable variation among countries.

For advanced economies, the focus should be on prioritizing AI innovation and integration while developing robust regulatory frameworks. In contrast, emerging markets and developing economies need to lay a strong foundation through investments in digital infrastructure and a digitally competent workforce. By doing so, we can cultivate a safe and responsible artificial intelligence environment that maintains public trust.

In the agricultural sector, artificial intelligence holds immense potential to address critical challenges faced by Africa, including low productivity, unpredictable climate conditions, and inadequate infrastructure. The integration of artificial intelligence technologies can bring about transformative changes in the agricultural sector.

For example, inprecision agriculture, AI-driven technologies such as drones and sensors provide real-time data on soil conditions, crop health, and weather patterns, enabling informed decision-making and resource optimization.

AI can also be used to optimize the supply chain with AI algorithms that can predict market demands, optimize logistics, and minimize post-harvest losses, benefiting farmers and contributing to national food security.

Insmart farming practices, AI-powered applications can assist farmers in remotely monitoring and managing their farms, from automated irrigation systems to predictive analytics for disease control.

Tailoring AI Adoption to African Realities

Contrary to concerns about global income inequality, Africa has the potential to bridge the gap through thoughtful AI integration in agriculture. Tailored solutions addressing crop diversity, regional climate variations, and socio-economic contexts are essential. Capacity building initiatives and investments in digital infrastructure, especially in rural areas, are imperative for successful AI adoption.

Despite IMF’s warning of potential inequalities, Africa can chart a different course by leveraging artificial intelligence to foster inclusive growth. The emphasis should be on empowering smallholder farmers, a significant portion of the agricultural workforce, with AI tools and knowledge. Governments, in collaboration with private stakeholders, can play a pivotal role in ensuring equitable distribution of AI benefits.

As Africa stands at a pivotal juncture, the transformative power of artificial intelligence in agriculture offers a unique chance to leapfrog traditional development barriers. Embracing artificial intelligence with a tailored approach can not only bridge technological gaps but also pave the way for building a resilient and prosperous agricultural future. In this AI-driven era, Africa has the opportunity to pioneer a sustainable and inclusive agricultural ecosystem that sets a global standard for progress and equity.

The ARCH Cold Chain Solutions Fund, with significant backing from the European Investment Bank (EIB), has introduced Africa’s first cutting-edge cold storage facility. Nestled within the Tatu City Special Economic Zone in Nairobi, Kenya, this facility, boasting a total investment of US$81 million, including a substantial US$15 million infusion from the EIB, promises to transform the food distribution landscape in East Africa. The main goal is to combat food waste and elevate safety standards in the region.

Spanning an expansive 17,700 square meters, the flagship facility is a marvel of design, offering unparalleled flexibility to accommodate a diverse array of products while operating seamlessly across various temperature ranges. With a storage capacity of up to 18,000 pallets—equivalent to a staggering 18,000 tons of perishable goods and pharmaceuticals at full tilt—the facility is envisioned to make a substantial impact on the region’s supply chain dynamics.

Setting itself apart, the facility is committed to adhering to the Leadership in Energy and Environmental Design (LEED) Standard, with aspirations for a coveted LEED Gold Certification. The European Investment Bank noted in a press release that, if achieved, this would mark a historic moment as the first facility in Africa to attain such recognition, signifying a significant stride in sustainable infrastructure development across the African continent.

According to IEB, the facility is committed to sourcing up to 30% of its energy needs from off-grid renewable power production, primarily leveraging solar photovoltaic technology to minimize its climate impact. The primary objective of the cold storage facility is to contribute to the reduction of food waste in East Africa.

According to data from the Food and Agriculture Organization of the UN (FAO), an alarming 37% of food produced in Sub-Saharan Africa is lost along the value chain. The ARCH Cold Chain Solutions Fund, through its state-of-the-art facility, aims to address this challenge by providing efficient cold storage and temperature-controlled solutions.

According to the Managing Director and Co-Head of ARCH Cold Chain Solutions East Africa Fund, the facility’s strategic expansion plan includes Mombasa, Kigali, Dar es Salaam, Addis Ababa, and Kampala, with an overall vision to reach a combined capacity of 100,000 tons in cold storage space.

The Head of the EIB Regional Hub for Eastern Africa expressed pride in supporting the ARCH Cold Chain Fund, highlighting the unique quality and flexibility offered by the facility for cold storage and acknowledging its role in reducing waste and setting global food safety standards in the region. The ARCH Cold Chain Solutions Fund is dedicated to developing and operating large-scale, energy-efficient cold chain solutions with a comprehensive logistics and distribution network across Eastern and Central Africa.

The recent East African Community (EAC) Heads of State Summit has ushered in a new era of commitment towards climate-smart policies and investments to fortify the agricultural sector across the continent. The consensus among the leaders is clear: by strengthening climate-smart agriculture and renewable energy, Africa can mitigate the adverse effects of climate change and ensure enhanced food access for its citizens.

One of the key focal points of the summit is the urgent need to augment rainwater harvesting for irrigation purposes, a vital component of sustainable agriculture. The leaders recognize that efficient water management is integral to addressing the challenges posed by climate change. As climate patterns shift, the availability of water for agricultural use becomes a critical factor, and investing in rainwater harvesting emerges as a practical solution.

The heads of state acknowledge the imperative to minimize post-harvest losses through the adoption of modern technologies. The integration of cutting-edge solutions for the storage and distribution of agricultural products is deemed crucial. Embracing these technologies not only ensures food security but also contributes to the economic sustainability of the agricultural sector.

A united stance was taken on the importance of expanding forest cover and safeguarding existing forests. The leaders see this as a strategic move to position the region favorably in carbon trading and climate financing on the global stage. By prioritizing environmental sustainability, the EAC aims to set an example for the rest of the world, emphasizing the interconnectedness of climate, forests, and economic prosperity.

The nations showcased innovative strategies, with Tanzania’s Build Better Tomorrow initiative focusing on engaging youth and women in agriculture through climate-smart technologies, promoting sustainability, and reducing poverty. Kenya’s commitment to conserving water towers and planting 15 billion trees aims to not only safeguard the environment but also tap into carbon trading for economic gains. On the other hand, Rwanda prioritizes collaboration between the government and the private sector, investing in infrastructure and cold storage to manage post-harvest losses.

Common Purpose for COP 28

The unified stance of approaching COP 28 as a bloc emphasizes Africa’s commitment to addressing climate change on the global stage. This solidarity ensures that the region’s development goals align with climate change mitigation efforts, fostering complementarity among partner states.

Kenya’s President William Ruto announced plans to privatize 35 state-owned companies, with an additional 100 under consideration, in what is termed a transformative step towards economic recovery. The decision comes at a crucial juncture for the East African nation, grappling with the aftermath of the COVID-19 pandemic, the aftershocks of the conflict in Ukraine, and a historic drought in the Horn of Africa.

President Ruto, speaking to investors on November 23, emphasized the government’s commitment to reducing bureaucracy and enhancing efficiency in the delivery of services. The move is seen as a response to the International Monetary Fund’s (IMF) recent call for reforms in state-owned enterprises, particularly highlighting the challenges faced by entities such as Kenya Power and Kenya Airways, both of which reported significant losses in 2022.

The Privatization Bill 2023, approved by the Kenyan Cabinet in March 2023, empowers the Ministry of Treasury to facilitate the sale of non-strategic parastatals without the need for parliamentary approval. This radical legislation aims to streamline the privatization process, allowing the private sector to play a more significant role in the nation’s economy.

“We have very lucrative (public) enterprises, but they are stifled by government bureaucracy, whereas the services they offer can be better provided by the private sector,” he asserted. The government’s proactive approach seeks to unleash the potential of these enterprises, positioning them for growth and increased competitiveness.

The revised law, signed into effect in October 2023, seeks to increase private sector participation, reduce the burden on government coffers, and foster economic resilience. Notably, the Privatization Commission will transform into the Privatization Authority, housed within the Treasury, overseeing the implementation of the sales.

Among the agricultural state-owned entities earmarked for privatization are Chemelil Sugar, South Nyanza Sugar, Nzoia Sugar, Miwani Sugar, Agro-Chemical and Food Company, Kenya Wine Agencies, and Kenya Meat Commission. Other companies include Kabarnet Hotel, Mt. Elgon Lodge, Golf Hotel, Sunset Hotel Kisumu, Kenya Safari Lodges and Hotels, Consolidated Bank, Development Bank of Kenya, and public universities, among others.

This move comes as part of the government’s broader strategy to address the country’s economic challenges. Kenya’s public debt reached over 10.1 trillion shillings at the end of June 2023, equivalent to around two-thirds of its gross domestic product. In response, the government has introduced a budget that includes new taxes, albeit facing resistance and protests from the public.

President William Ruto’s government has secured financial support from various international institutions, including the IMF and the World Bank, further raising the country’s debt ceiling. On November 16th, the IMF announced that it had finalized an agreement for a loan of $938 million for Kenya, as the nation faces the upcoming repayment of a $2 billion Eurobond in 2024. At the same time, on November 20th, the World Bank disclosed its intentions to extend a financial support package of $12 billion to Kenya over the course of the next three years.

Despite public skepticism about his economic recovery plans, judging from his remarks, President Ruto remains bullish about the privatization initiative, which is expected to generate much-needed revenues, reduce conflicts between regulatory and commercial functions, and spur growth in the capital markets.

A transformative breakthrough is unfolding for cashew nut farmers in the coastal Arid and Semi-Arid Lands (ASAL) in Kenya. The visionary initiative comes from an economic diversification program aimed at establishing cashew nut nurseries and farms in these regions.

The State Department for Crop Development has been stalwart in advancing agricultural technologies, initially launching four new cashew nut varieties that boast drought tolerance, disease resistance, and a remarkable one-and-a-half-year maturation period, in stark contrast to traditional varieties taking five years. Named Kkrorosho75, Kkorosho 81, Kkrosho 82, and Kkrosho 100, these varieties are set to improve farmers’ earnings by enabling quicker planting, harvesting, and selling cycles.

Cashew nut farming is a good opportunity for Kenyans who want to cultivate in arid areas because it does not require a lot of rain and is drought-tolerant.

However, the industry has been facing unique challenges that saw most of the cashew nut farmers abandon the enterprise for other ventures due to diseases, pricing and climate change challenges that mostly affected the conventional varieties.

The Kenya Agricultural and Livestock Research Organization (KALRO) has previously stated that the newly developed cashew nut varieties have the capability to address the challenges previously faced by farmers since they are tolerant to major cashew nut diseases and are resilient to adverse weather conditions since they require minimal water. The new varieties are also said to fetch higher market prices, ranging from about 50-70 Kenya Shillings per kilogram, a significant improvement from the earlier rates of 10 to 20 Kenya Shillings.

According to KALRO, the cashew nut industry supports around 50,000 people, with a production of 10,000 metric tonnes. The demand for cashew nuts far exceeds the current production, presenting a lucrative opportunity for farmers to capitalize on the market, both locally and abroad.

Historically, veteran cashew nut farmers in coastal regions had heydays as it was the main economic activity. However, political interference and mismanagement led to the decline of the once-thriving Kenya Cashew Nut Limited, impacting farmers’ livelihoods.

The closure of the processing factory in 1990 dealt a severe blow to the industry, prompting farmers to cut down their cashew nut trees. The void left by the processing plant allowed middlemen to exploit farmers, controlling prices to the detriment of those dependent on cashew nut farming.

To address these challenges and breathe new life into the cashew nut industry, a comprehensive 360-degree approach is needed for implementation of a cashew nut enhancement productivity program, focusing on annual seedling planting, training of farmers, establishing cottage industries to discourage the exportation of raw nuts, value addition, and marketing.

It will take concerted efforts from all stakeholders in order to fully revive the cashew nut industry, with the need for policy direction, organized farmer groups, and strategic investments.

Scientists from the University of Chicago have uncovered the immune-boosting potential of trans-vaccenic acid (TVA), a fatty acid abundant in beef, lamb, and dairy products. This discovery, published in Nature, sheds light on how TVA enhances the effectiveness of immune cells, specifically CD8+ T cells, in infiltrating tumors and combating cancer cells.

Lead researcher Professor Jing Chen, along with colleagues Hao Fan and Siyuan Xia, embarked on a meticulous exploration into the impact of nutrients on anti-tumor immunity. Their work, detailed in the publication, unveils TVA as a standout candidate among 255 bioactive molecules screened for their ability to activate CD8+ T cells. Intriguingly, TVA, found in substantial quantities in human milk and derived from grazing animals, demonstrated superior performance in both human and mouse cells.

The study’s significance extends beyond the laboratory, as the team conducted experiments feeding mice a diet enriched with TVA. The results were striking—tumors, particularly melanoma and colon cancer cells, exhibited reduced growth potential compared to mice on a control diet. Additionally, CD8+ T cells displayed enhanced infiltration into tumors, showcasing TVA’s potential in augmenting the body’s natural defenses against cancer.

Delving deeper into the molecular realm, the researchers harnessed innovative techniques such as kethoxal-assisted single-stranded DNA sequencing (KAS-seq) to uncover how TVA influences cellular processes. Their findings revealed that TVA inactivates the GPR43 receptor on cell surfaces, outperforming short-chain fatty acids often produced by the gut microbiota. This activation triggers the CREB pathway, a cellular signaling process crucial for growth, survival, and differentiation.

The team also analyzed blood samples from lymphoma patients undergoing CAR-T cell immunotherapy. Strikingly, patients with higher TVA levels exhibited more favorable responses to treatment. Similarly, testing leukemia cell lines demonstrated TVA’s ability to enhance the effectiveness of immunotherapy drugs against leukemia cells.

Despite these promising findings, Professor Chen emphasizes caution regarding dietary implications. While TVA shows potential as a dietary supplement for T cell-based cancer treatments, the emphasis should be on optimizing the nutrient itself rather than increasing consumption of red meat and dairy, which have known health risks. Professor Chen anticipates that other nutrients, possibly from plant sources, may also activate the CREB pathway, opening avenues for further research.

This new research elaborates on the potential of a “metabolomic” approach to understanding how dietary components impact health. Professor Chen and his team aspire to construct a comprehensive library of nutrients circulating in the blood to understand their impact on immunity and broader biological processes, including aging.

The Kenyan government, through the Kenya Dairy Board (KDB), has unveiled a 10-year plan, the Kenya Dairy Industry Sustainability Roadmap 2023–2033, aimed at doubling dairy farmers’ income by increasing milk production per cow. The announcement was made by Mithika Linturi, the Cabinet Secretary for Agriculture and Livestock Development, during a launch event in Nairobi.

Linturi emphasized that the primary goal of the government is to raise annual milk production from the current five billion liters to an impressive 10 billion liters. The strategy includes a plan to increase dairy exports to one billion liters, elevate the formally marketed milk percentage from 30% to 50%, and boost the monthly revenue of small-scale dairy farmers to 56,000 Kenya Shillings.

The CS outlined key interventions to achieve these targets, focusing on improved access to fodder and feeds. The roadmap seeks to double the daily milk productivity per cow, addressing the challenge of the current yield per cow, which is below seven liters per day and falls short of global standards.

With an estimated dairy herd population of 5.1 million and over two million smallholder dairy farmers, Kenya currently produces 5.2 billion liters of milk annually, valued at over 230 billion Kenya Shillings. Linturi stressed the importance of enhancing productivity and noted that doubling production per cow is a more practical approach than increasing the size of the dairy herd.

To achieve this, the CS stressed the significance of providing better feeds, veterinary services, and a clean environment, with observable results in less than a week. He acknowledged that low productivity, high production costs, and other inefficiencies have hindered the industry’s potential.

In a bid to address environmental concerns, Linturi revealed the government’s commitment to reducing greenhouse gas emissions from the dairy sector by 0.4 Metric tonnes of CO2 equivalent by 2030. He highlighted ongoing collaborative efforts, including the “Pathways to Dairy Net Zero” (PADNET) project, developed in partnership with the State Department of Livestock Development, Kenya Dairy Board, UN, FAO, and IFAD.