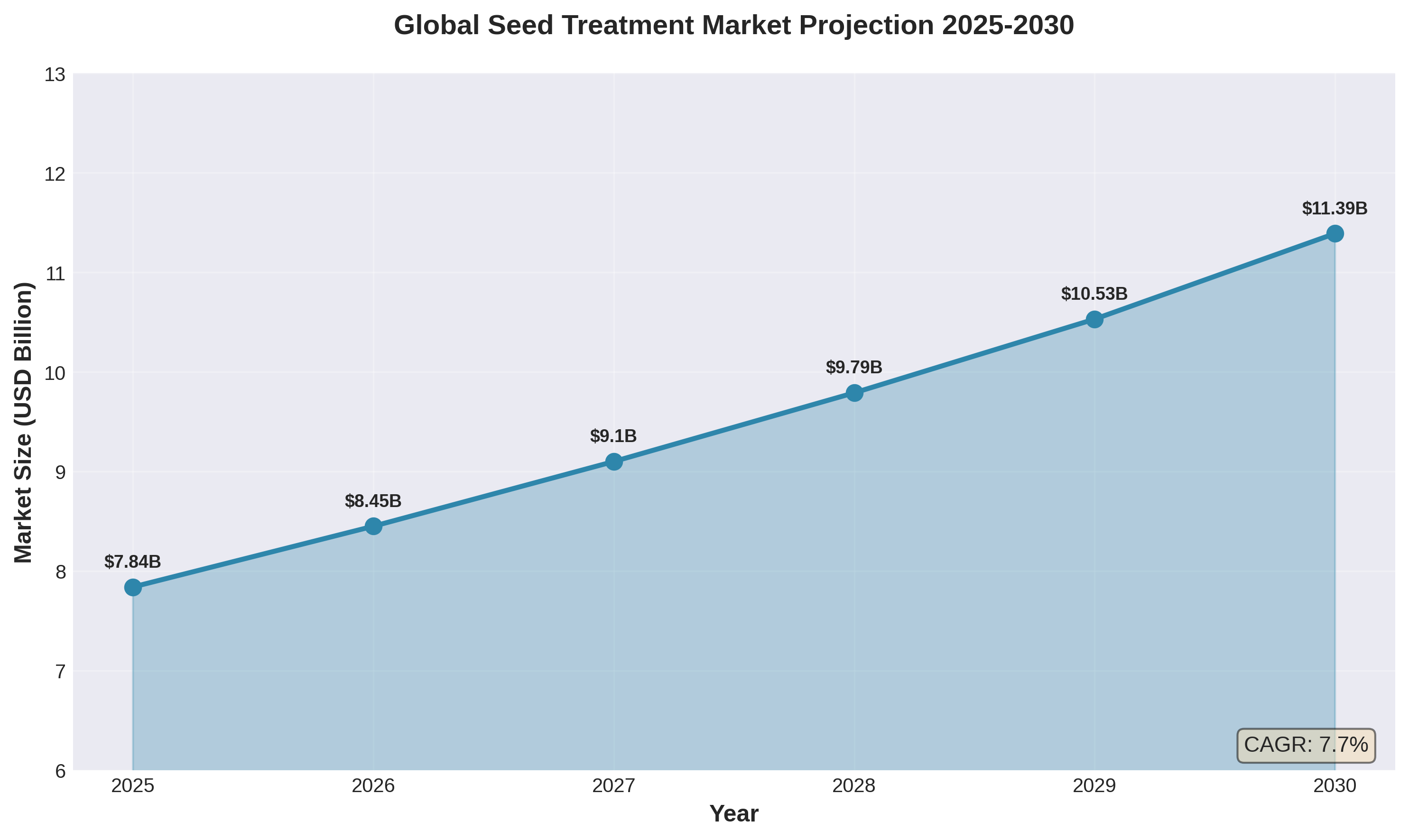

The global seed treatment market is entering a period of sustained expansion driven by population growth and the push for sustainable agriculture. Industry estimates project the market will reach between $11 billion and $12 billion by 2030, with biological solutions gaining ground over traditional chemical treatments.

Market Growth Trajectory

The seed treatment industry demonstrates consistent upward momentum, with a compound annual growth rate (CAGR) of 7.7% from 2025 to 2030. This growth reflects increasing recognition of seed treatments as cost-effective interventions that deliver outsized benefits during critical early crop development stages.

Rising Food Demand Fuels Market Growth

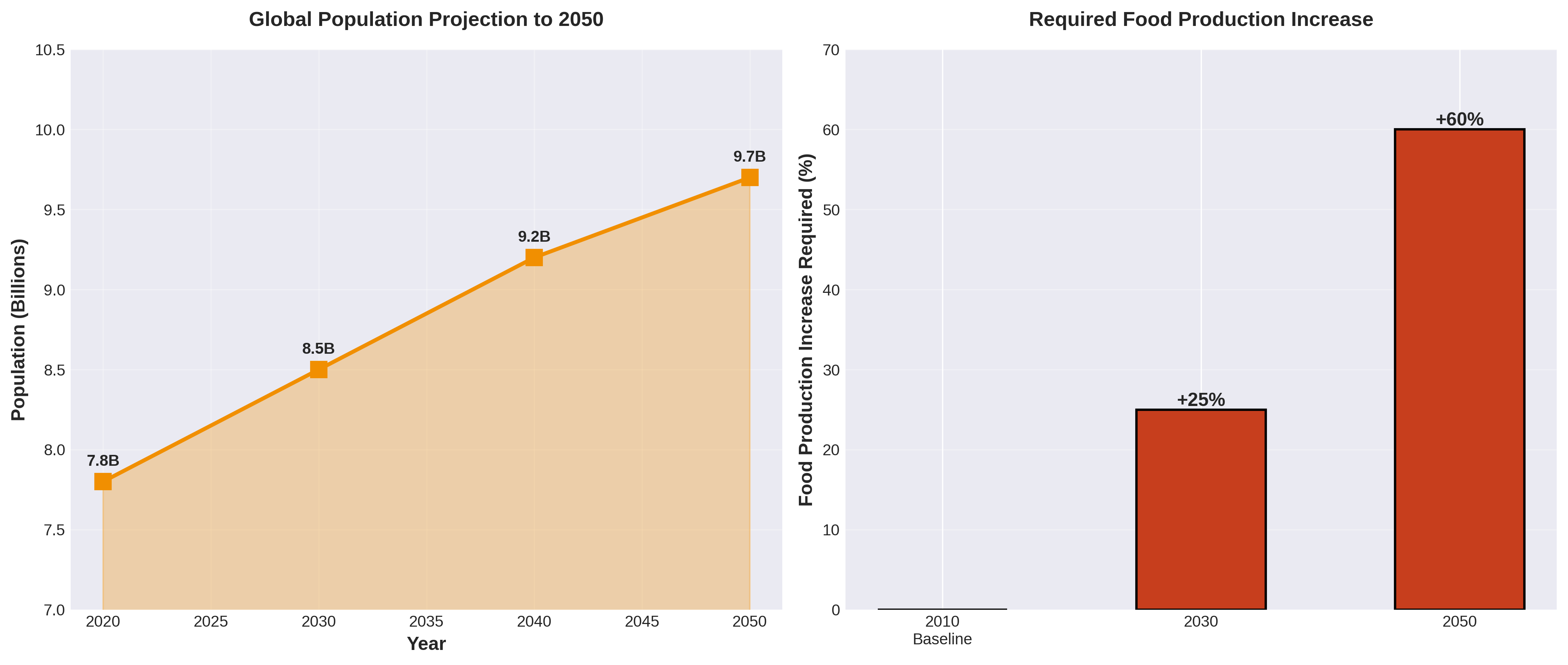

With global population expected to reach 9.7 billion by 2050, agricultural production must increase by approximately 60% to meet food demand. Seed treatments address this challenge by protecting seeds during vulnerable early growth stages, improving germination rates, and improving crop establishment.

The dual pressure of population growth and the need for increased food production creates sustained demand for agricultural technologies that enhance crop productivity. Seed treatments offer a targeted solution, delivering protection and growth enhancement precisely when crops are most vulnerable.

Regional Market Distribution

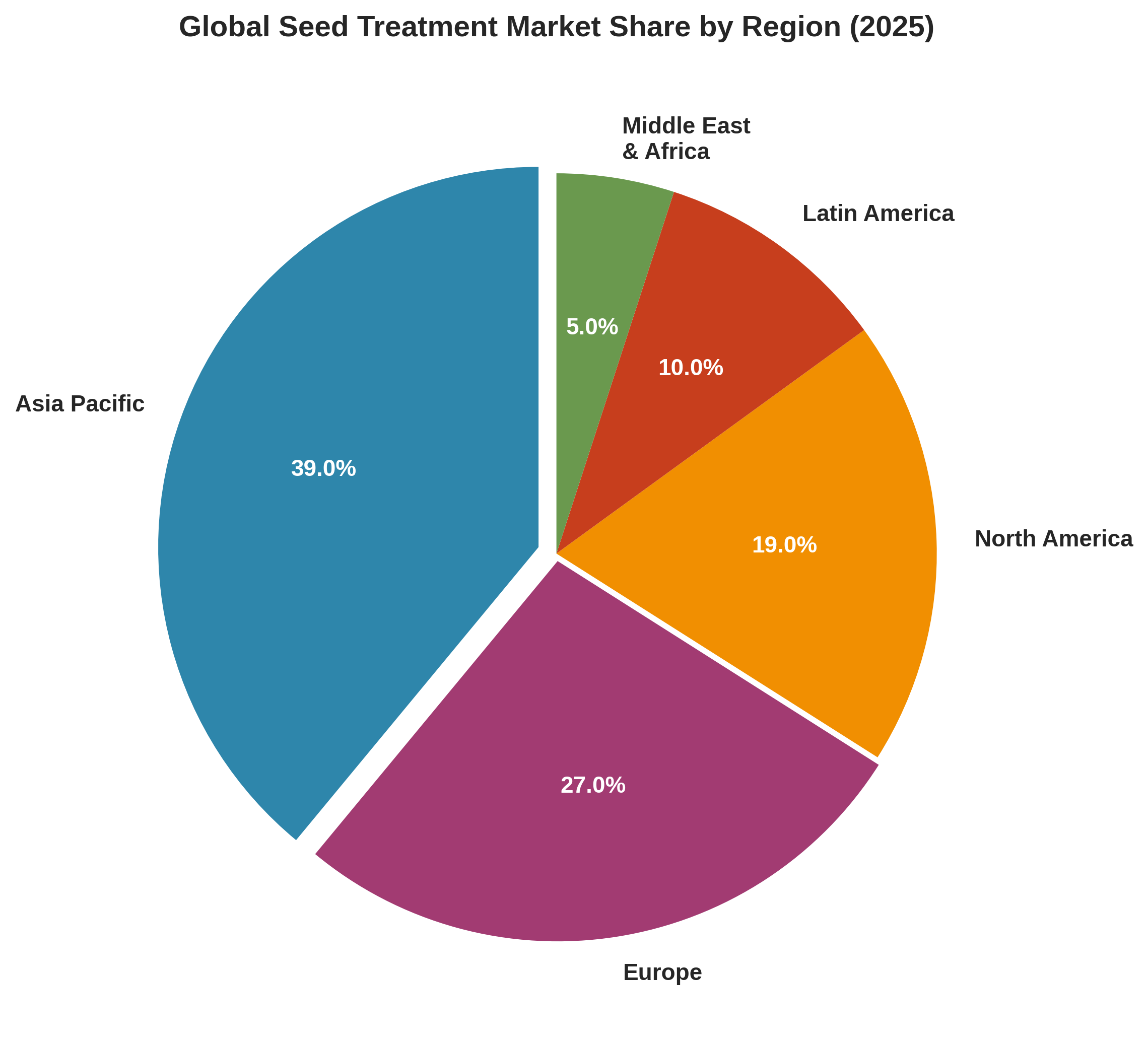

Asia Pacific leads the market, with Europe and North America following as significant regional players. The shift reflects both agricultural scale in developing regions and advanced farming practices in established markets.

Asia Pacific's dominance at 39% of global market share stems from vast arable lands, rising populations, and increasing adoption of modern agricultural practices in countries including India and China. Europe's 27% share reflects stringent environmental regulations driving innovation in biological treatments, while North America's 19% represents advanced precision agriculture adoption.

Biological Treatments Gain Momentum

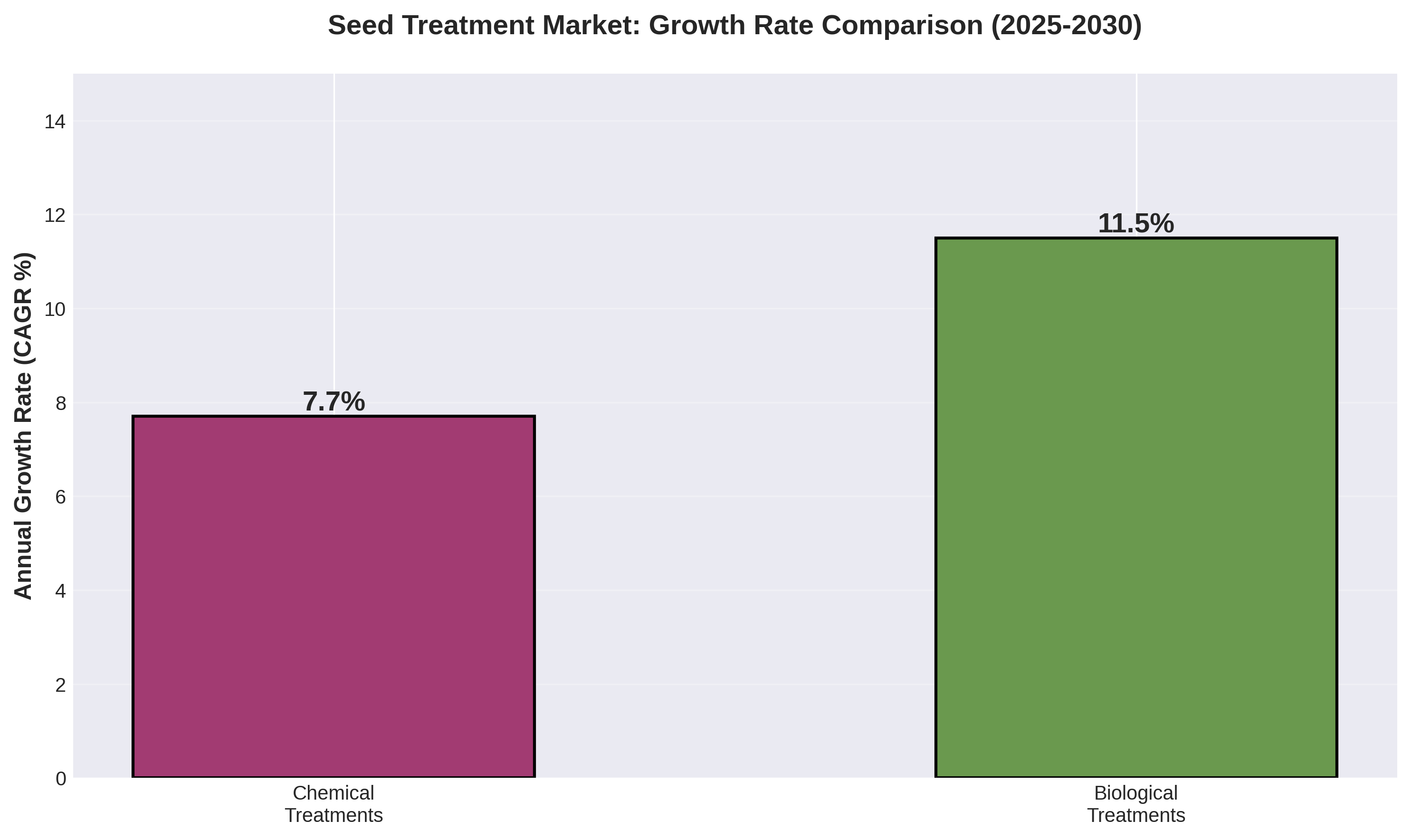

The biological seed treatment segment is growing at approximately 11-13% annually, outpacing traditional chemical treatments. This growth stems from stricter regulations on chemical pesticides, particularly in Europe where the EU is phasing out various chemical-based treatments.

Recent product launches demonstrate this trend:

July 2025: Bayer introduced Yoalo, a biostimulant seed treatment for corn based on Bacillus velezensis, designed to enhance early crop performance while reducing agrochemical dependence.

January 2025: UPL launched AtroForce, a bionematicide for cotton using Trichoderma atroviride to protect against nematode damage that contributes to yield losses in cotton fields.

August 2025: Australian agtech firm Loam Bio unveiled FurrowMate at AgQuip, a direct air injection system for applying biological treatments that eliminates messy manual seed coating processes.

Segment Performance

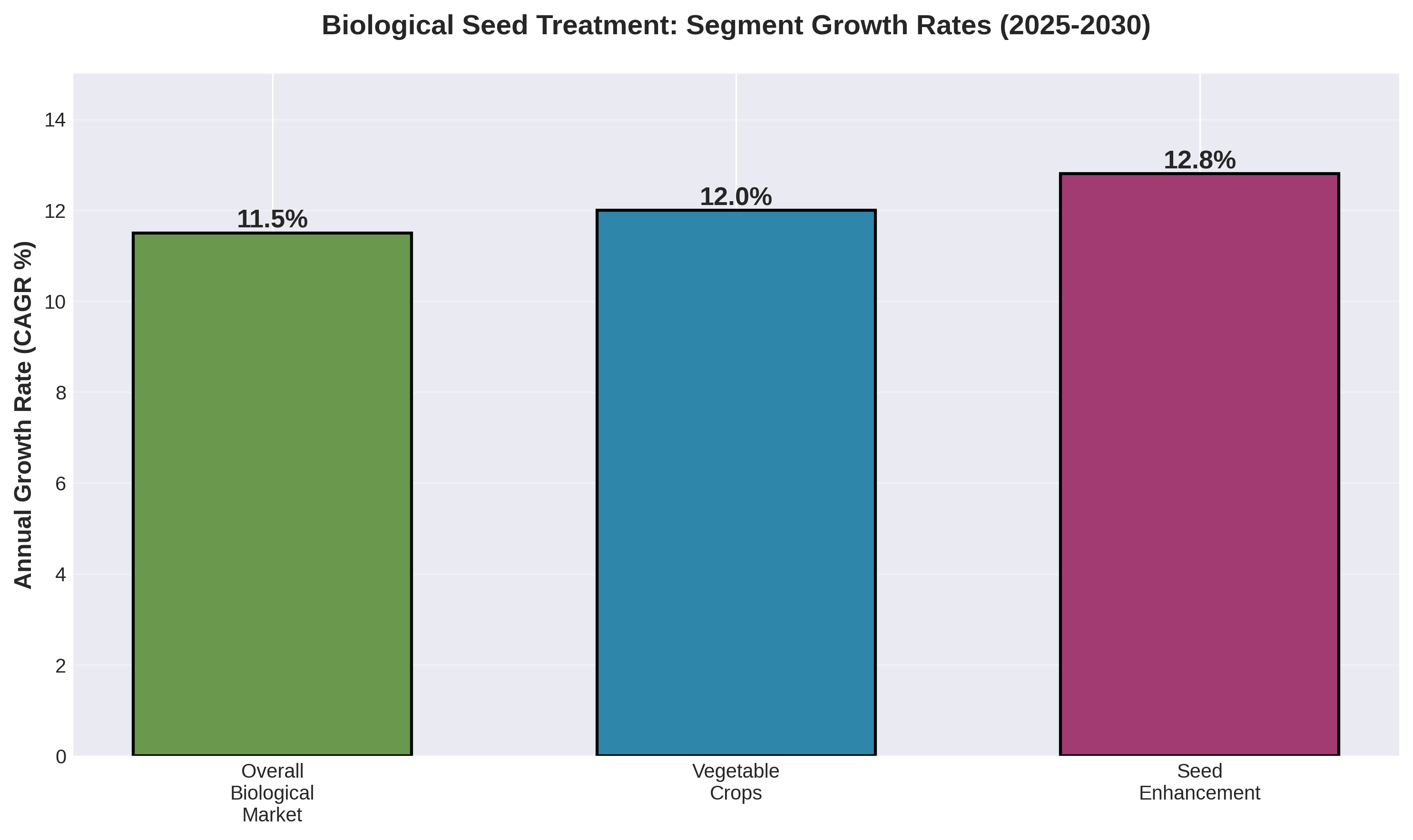

Within the biological seed treatment market, specific segments show accelerated expansion. The vegetable crop segment leads with a 12% growth rate, driven by consumer demand for organic produce and stricter pesticide regulations. Seed enhancement products, which integrate growth promotion and stress tolerance, represent the fastest-growing category at 12.8% CAGR through 2030.

Market Challenges and Opportunities

High costs remain a barrier, particularly for smallholder farmers in developing countries. However, corn treated with appropriate biological seed treatments can yield up to 10% more, providing economic incentive for adoption.

The vegetable crop segment shows rapid expansion at approximately 12% growth rate, driven by consumer demand for organic produce and stricter pesticide regulations. Protected cultivation systems increasingly require biological treatments as they offer effective disease protection while promoting robust plant development.

Technology and Sustainability Drive Innovation

Precision application technologies, including nano-encapsulation and automated seed coating systems, are improving treatment uniformity and reducing waste. These advances allow more targeted delivery of active ingredients while minimizing environmental impact.

The European Union's comprehensive sustainable agriculture programs and regulatory frameworks specifically designed for biological agricultural inputs reflect broader commitment to environmental stewardship. This regulatory environment creates both challenges for chemical treatments and opportunities for biological alternatives.

Market Outlook

The seed treatment market evolution mirrors broader agricultural transformation toward sustainability. As regulatory pressures increase and biological formulations improve, the industry continues adapting to meet global food security needs while reducing environmental footprint.

Key factors shaping the market through 2030:

Regulatory Environment: Continued phase-out of chemical pesticides in major markets drives biological innovation

Precision Agriculture: Integration with digital farming tools enhances treatment efficiency

Climate Resilience: Seed treatments that enhance stress tolerance gain importance

Sustainability Mandates: EU Farm to Fork Strategy and similar programs accelerate biological adoption

Economic Viability: Demonstrated yield improvements justify premium pricing for advanced treatments