From the maize fields of Kenya to the wheat plains of Argentina, from rice paddies in Bangladesh to soybean operations in Iowa—farmers worldwide face a common challenge in 2025: squeezed margins, volatile prices, and rising input costs. Yet within this turbulence, opportunities exist for those prepared to act.

The numbers tell a sobering story. Global fertilizer prices have surged 15% since January 2025, with urea up 36% and diammonium phosphate (DAP) climbing 23%. Meanwhile, grain prices have declined sharply from their 2022 peaks—corn down over 50%, soybeans down nearly 60% in major markets.

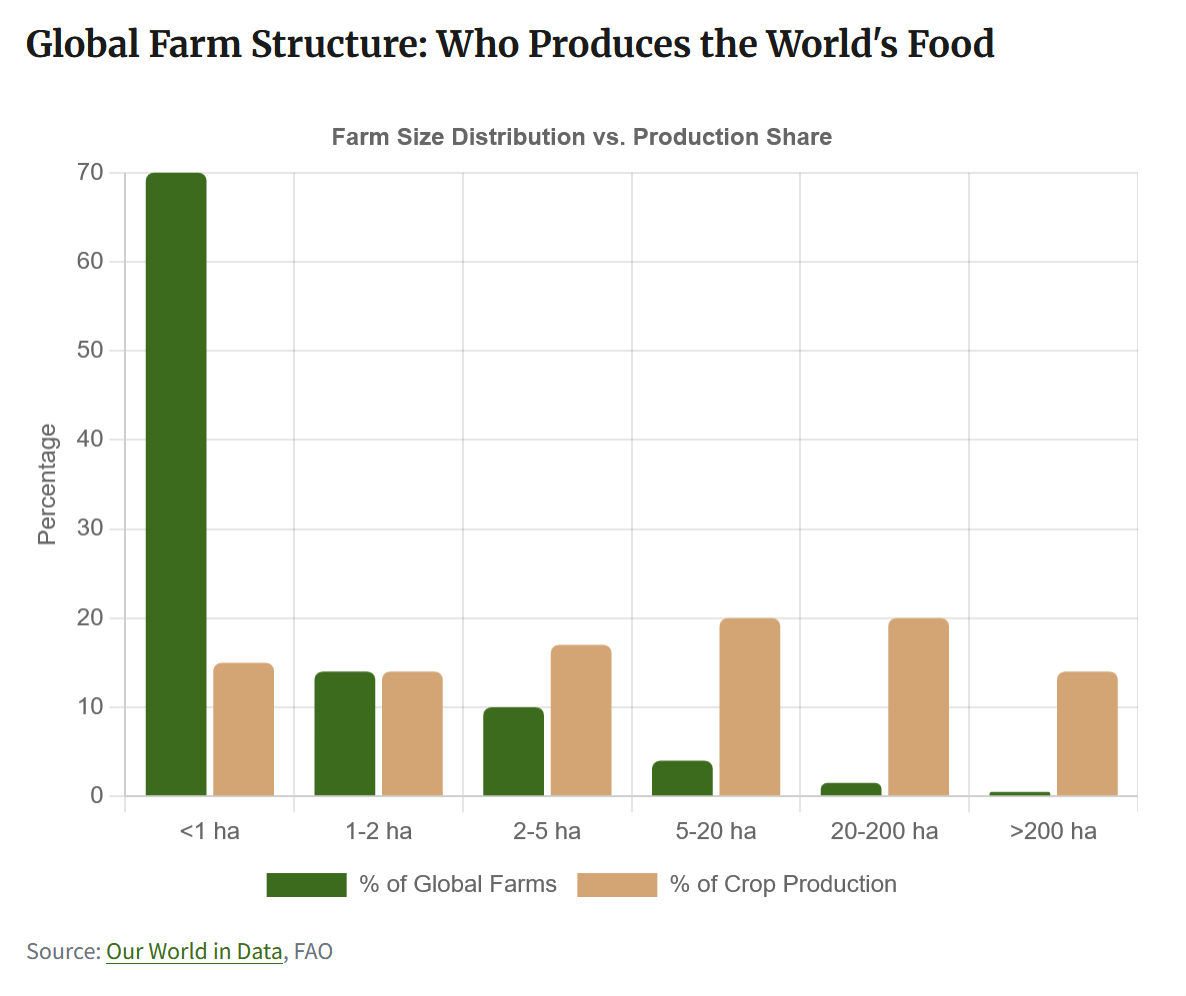

The squeeze affects everyone, but not equally. The world's 570 million smallholder farms—operating on less than two hectares—produce roughly one-third of global food. These farmers, concentrated in Asia (74%) and Sub-Saharan Africa, face the harshest pressures with the fewest tools to respond.

The Great Trade Shift: New Winners, New Losers

Global grain trade has been fundamentally reshaped. China—the world's largest soybean importer—has dramatically shifted purchases away from the United States toward South America. From January through August 2025, U.S. soybean exports to China totaled just 218 million bushels, down from 985 million during the same period in 2024.

Brazil now supplies approximately 65-80% of China's soybean imports, with total South American production reaching 230 million tons in 2024/25. This shift creates opportunities for some and challenges for others—but the underlying lesson applies globally: market access can change rapidly.

.png?alt=media&token=5c766657-5492-42f7-9030-0bedf3141243)

Input Costs: A Global Squeeze

The World Bank reports that fertilizer affordability—measured by the ratio of fertilizer prices to crop prices—has worsened significantly in 2025. DAP is now less affordable than it was during the 2022 crisis peak. China's export restrictions have cut nitrogen fertilizer exports by over 90%, tightening global supply.

This hits different regions differently. In Sub-Saharan Africa, where fertilizer use is already the lowest of any region, higher prices push even more farmers toward zero application—widening the yield gap. Average African cereal yields sit at 1.7 tonnes per hectare versus 4 tonnes globally and over 6 tonnes in North America.

Regional Realities, Universal Principles

While specific market conditions vary by region, certain principles apply universally: timing purchases strategically, reducing post-harvest losses, building local market relationships, and staying alert to price opportunities.

🌍 Sub-Saharan Africa

Key challenges: Post-harvest losses of 20-30% erase potential income before crops reach market. Only 4% of cropland is irrigated. Limited access to formal credit.

Opportunity: Hermetic storage bags and improved silos can reduce losses by 80%+. Warehouse receipt systems, where available, provide both storage and credit access. Group marketing through cooperatives captures better prices than individual sales.

🌏 South & Southeast Asia

Key challenges: Fodder prices in India have surged over 30%. Farmers receive just one-third of final prices, with intermediaries capturing the rest. Climate variability disrupts planting cycles.

Opportunity: Direct market linkages through farmer producer organizations bypass intermediaries. Government support programs (like India's urea subsidies) reduce input costs—understand and access what's available in your country.

🌎 Latin America

Key challenges: Despite being a major exporter, 41 million people in the region faced hunger in 2024. Currency volatility affects input costs. Climate events (La Niña) threaten production.

Opportunity: Counter-seasonal production for Northern Hemisphere markets. Brazil's dominance in soybean exports to China demonstrates how trade shifts can create new market access. Regional trade through AfCFTA-style agreements reduces dependence on distant markets.

🌐 North America, Europe, Australia

Key challenges: Production expenses hit record $467 billion in the U.S. in 2025. Commodity prices sit below production costs for many growers. Export markets have shifted.

Opportunity: Basis trading captures local premiums. Seasonal fuel purchases (winter for diesel, late summer for propane) reduce operating costs. Options strategies provide downside protection. Government support programs offset some losses.

.png?alt=media&token=99b7c824-05c8-4592-ac54-0be03c41ee17)

Practical Strategies by Farm Scale

Smallholder (<2 ha)

Reduce losses first: Hermetic storage can save 20-30% of harvest value

Join cooperatives: Collective bargaining power improves prices

Diversify crops: Multiple crops spread risk across seasons

Access support programs: Many countries subsidize inputs—know what's available

Local markets first: Direct sales often yield better returns than commodity channels

Small-Scale (2-20 ha)

Time input purchases: Fertilizer and fuel prices follow seasonal patterns

Build storage capacity: Ability to hold grain enables better timing

Forward contracts: Lock in prices before harvest when favorable

Monitor local basis: Price differences between locations create opportunity

Invest in quality: Premium prices often available for certified or graded grain

Large-Scale (20+ ha)

Hedge with options: Put contracts establish price floors

Strategic fuel buying: Lock in diesel/propane during seasonal lows

Diversify markets: Multiple buyers reduce single-customer risk

Monitor geopolitics: Trade policy shifts create rapid price movements

Precision application: Variable-rate technology optimizes input use

The Universal Principle

Regardless of scale or region, farmers who capture value do three things consistently: they reduce what they lose (storage, timing), they control what they spend (strategic input purchasing), and they stay alert to what the market offers (local premiums, timing windows). These fundamentals transcend geography.

Timing Matters: Seasonal Opportunities

Global commodity markets follow patterns. Understanding these cycles creates opportunity regardless of where you farm.

Grain prices typically bottom at harvest when supply floods the market, then strengthen through storage season as grain moves into consumption. Nine years out of ten, corn prices hit their low during fall harvest. For Southern Hemisphere farmers, this pattern reverses—Brazilian soybean harvests in February-March often pressure global prices, creating buying opportunities for Asian and African importers.

Fuel costs follow heating and planting demand. Propane prices typically dip in late summer before winter heating demand. Diesel often peaks before planting and harvest seasons. Buying outside these windows saves 5-10%.

Fertilizer demand peaks before planting seasons in major producing regions. Global demand reached 200 million tons in 2024/25, just below record highs. Prices typically ease slightly after peak demand periods—though 2025's supply constraints have muted this pattern.

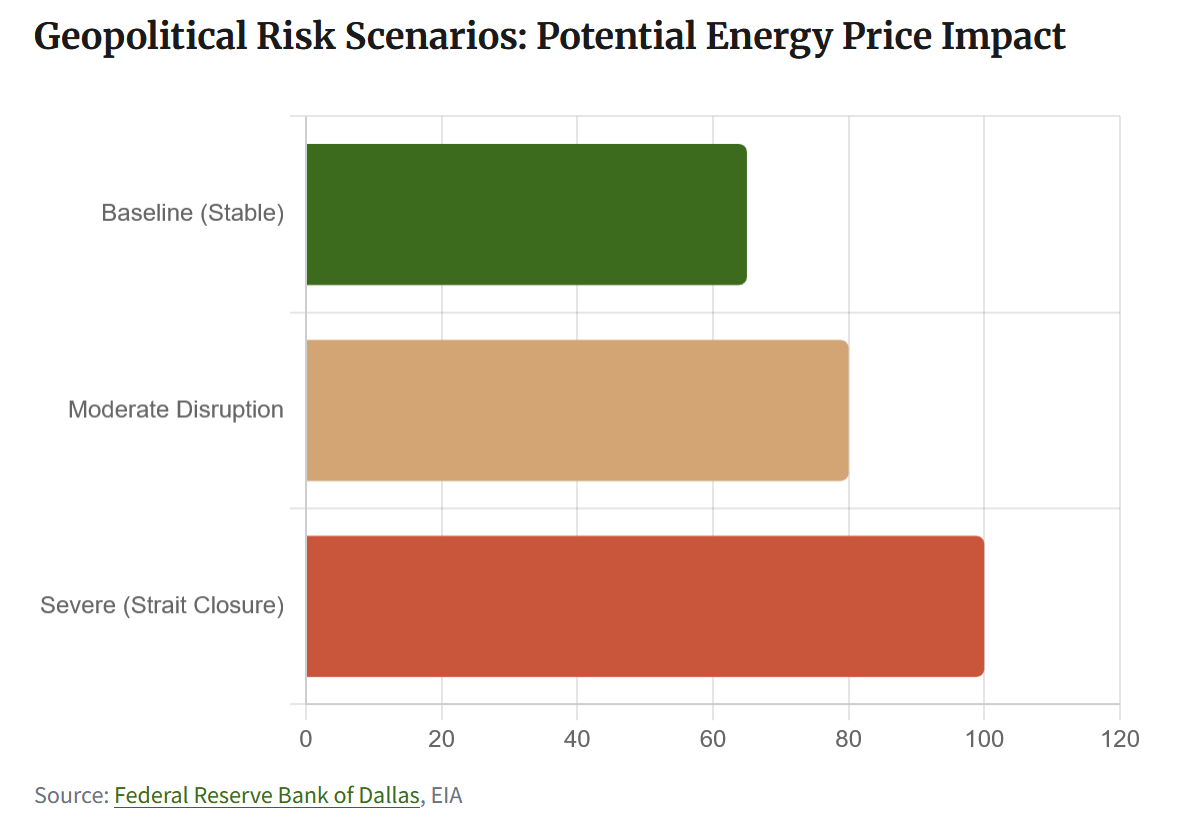

Geopolitical Risk: What to Watch

Energy and agricultural markets remain sensitive to geopolitical developments. The Russia-Ukraine conflict continues to affect wheat and fertilizer flows. Middle East tensions create oil price risk that ripples through to fuel and nitrogen fertilizer costs. U.S.-China trade tensions reshape soybean flows.

For farmers, the practical implication is clear: events far from your fields can move your prices. Those who monitor global developments—not to predict them, but to respond quickly when they occur—capture opportunities others miss.

The Path Forward

The OECD-FAO Agricultural Outlook projects continued price volatility through the decade, driven by weather shocks, supply chain disruptions, and geopolitical tensions. Real commodity prices are expected to decline modestly as productivity improves—but this puts pressure on individual farmers to improve their own efficiency to remain competitive.

For smallholders, this means pursuing every available support program, reducing losses, and building market access through collective action. For commercial operations, it means aggressive cost management, strategic timing, and diversified marketing. For all farmers, it means staying informed and prepared to act when opportunities emerge.

"Sustained improvements in agricultural efficiency, adoption of innovative technologies, and better access to inputs, knowledge, and markets are critical for maintaining farm incomes and livelihoods." — OECD-FAO Agricultural Outlook 2025-2034

Market chaos creates both risk and opportunity. The farmers who thrive will be those who prepare for both.