From smallholder farmers in sub-Saharan Africa to large-scale operations in the American Midwest, agricultural producers worldwide face a common challenge: declining incomes amid rising costs. The pressures differ by region and scale, but the fundamental squeeze between input costs and commodity prices threatens farm viability across continents.

The Global Picture

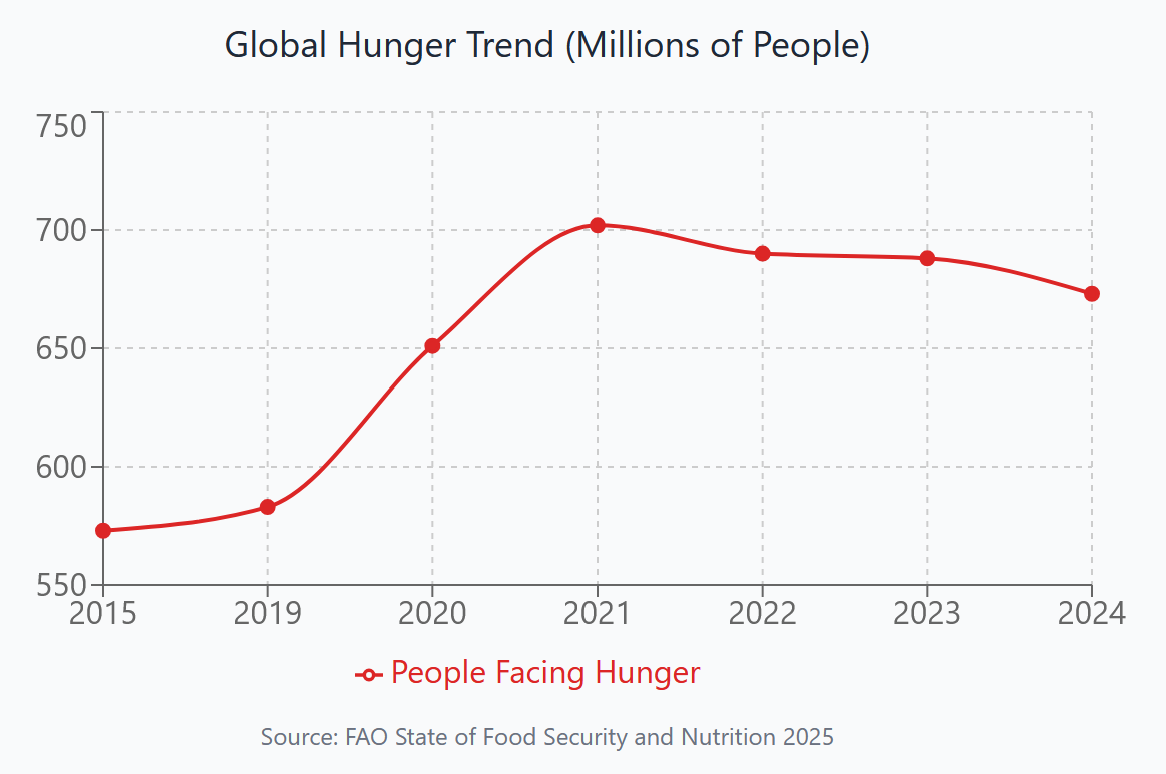

The world's 570 million farms feed humanity, yet those who grow our food increasingly struggle to earn a living. According to FAO data, approximately 673 million people experienced hunger in 2024—90 million more than in 2020. Paradoxically, many of these hungry people are farmers themselves. The 2025 State of Food Security report found that food insecurity is more prevalent in rural areas, affecting 32% of adults—compared to 26% in urban zones.

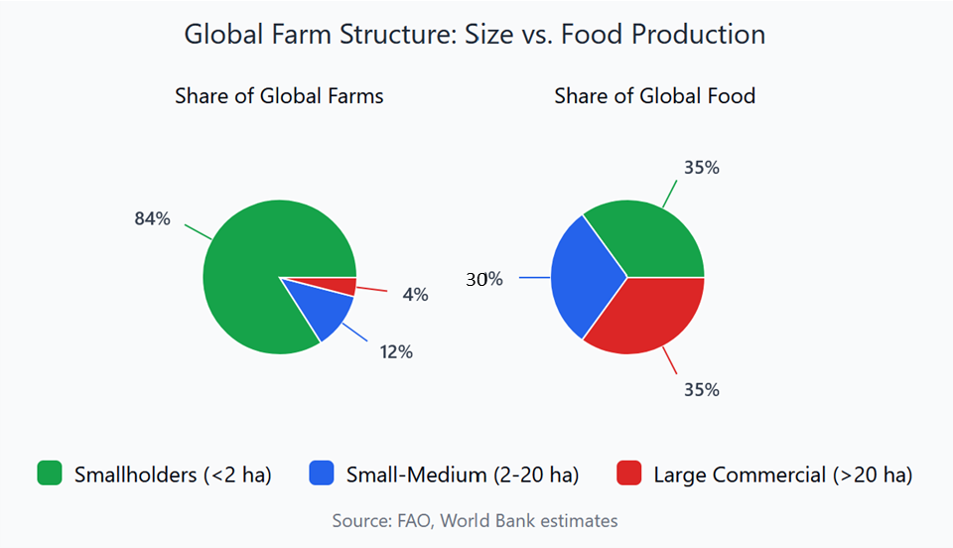

Smallholder Farmers: 84% of Farms, 35% of Food

Research published in PNAS analyzing 55,000 smallholder farms across six African countries found that crop productivity declined 3.5% annually from 2008-2019—the opposite of what development goals require. In a study of Cambodian smallholders, 92% of farmers reported declining household income, with 63% forced to cut expenses.

These figures matter because smallholders produce up to 80% of food consumed in Asia and sub-Saharan Africa. Farms under 2 hectares represent 84% of the world's farms, yet their operators face barriers that larger operations do not: limited market access, inadequate credit, poor infrastructure, and minimal technical support.

Commercial Agriculture Under Pressure

Large-scale commercial farmers face different but equally serious challenges. In the United States, net farm income fell nearly 30% from 2022's peak of $181.9 billion to $127.8 billion in 2024. Chapter 12 farm bankruptcies rose 55% in 2024, with filings in early 2025 tracking 70% above the prior year.

Canada's Net Cash Income declined 7% in 2024 with a further 15% drop forecast for 2025. In Brazil, several large producers declared bankruptcy in early 2024 following drought losses, according to industry reports. The European Union has lost over 5 million farms since 2005, with two-thirds of remaining farmers reporting diminished investment capacity.

The Cost-Price Squeeze

A 2024 McKinsey survey found that 48% of farmers globally cited input costs—fertilizer, seeds, crop protection—as their primary concern, up from previous years. Climate and weather risk ranked second at 41%, up from 35% in 2022.

.png?alt=media&token=b7a392da-a154-4a51-be14-96fe8384f805)

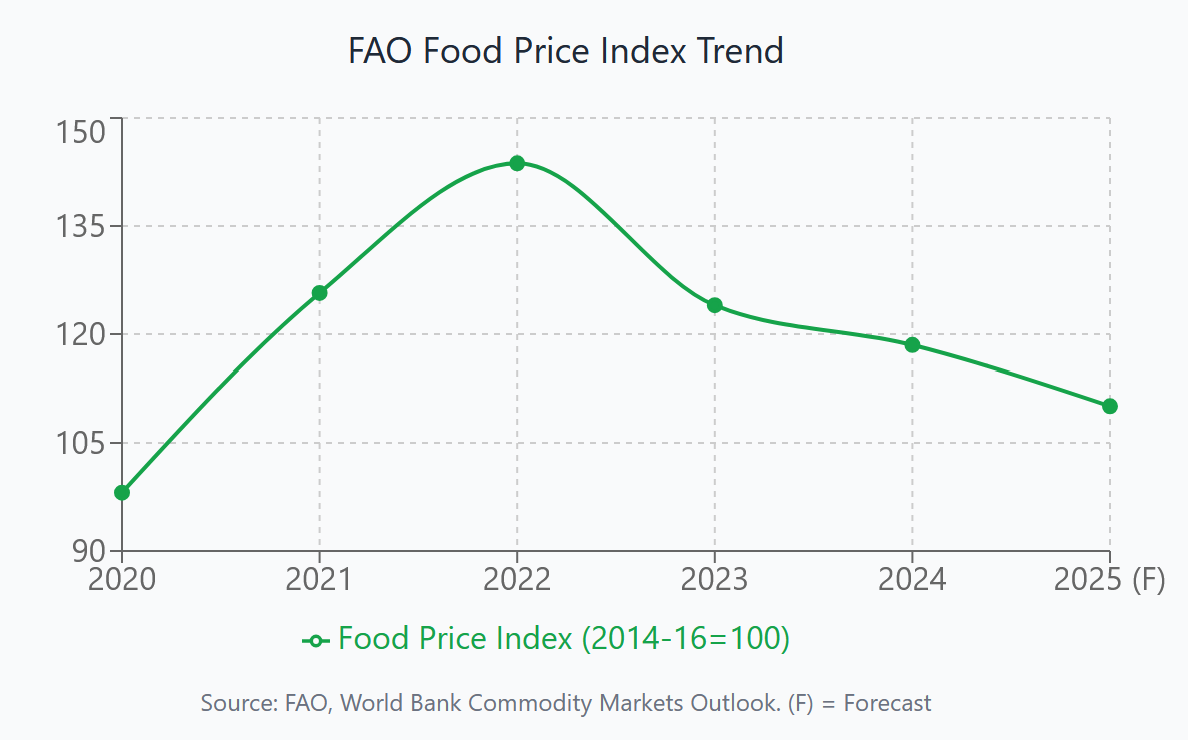

While input costs remain elevated, commodity prices have fallen. The World Bank projects global food prices to decline 6-7% in 2025, with further softening through 2026. The FAO Food Price Index stood at 126.4 in October 2025—down 27% from peak levels.

Climate Disasters: $3.26 Trillion Lost

The FAO's 2025 Impact of Disasters report documents $3.26 trillion in agricultural losses from disasters over 33 years—an average of $99 billion annually, or 4% of global agricultural GDP. Africa suffers the highest relative burden, losing 7.4% of agricultural GDP to disasters despite lower absolute losses. Between 1991 and 2023, disasters destroyed 4.6 billion tonnes of cereals, 2.8 billion tonnes of fruits and vegetables, and 900 million tonnes of meat and dairy.

.png?alt=media&token=80725a52-ad96-4a2c-b213-6259d5365ac1)

Strategies That Work Across Scales

Despite regional differences, successful adaptation strategies share common elements:

Diversification reduces vulnerability. This applies universally. For smallholders, it may mean intercropping, integrating livestock with crops, or adding agroforestry. For commercial operations, diversification might involve rotating crops, entering livestock production, or developing agritourism. Diversified farms consistently outperform single-commodity operations in downturns.

Market access determines income capture. Research from J-PAL confirms that farmers with better market connections—whether through cooperatives, digital platforms, or direct buyer relationships—capture more value from their production. This applies to smallholders selling through village aggregators and commercial farms negotiating forward contracts.

Climate-smart practices build resilience. Whether drought-tolerant seed varieties for African smallholders or precision irrigation for large operations, matching production practices to local climate realities protects yields. In India, the Minimum Support Price system provides floor prices for 23 crops, though effective reach remains limited.

Financial planning and risk management matter at every scale. For smallholders, this may mean index-based crop insurance delivered via mobile phone—initiatives now reaching millions of African farmers through digital platforms. For commercial operations, it means maintaining debt-to-asset ratios that provide flexibility during downturns and timing credit conversations before distress becomes acute.

Collective action amplifies individual capacity. Cooperatives, farmer organizations, and producer groups provide smallholders with bargaining power, shared infrastructure, and knowledge exchange that individual farms cannot achieve alone. In Latin America, precision agriculture adoption exceeds 60% in Argentina partly due to farmer networks sharing technology and expertise.

The Path Forward

The challenges facing farmers worldwide are structural, not cyclical. Climate volatility is intensifying. Input costs remain elevated. Commodity price support programs in many countries have not kept pace with production realities. Yet every $1 invested in anticipatory action against agricultural disasters generates up to $7 in benefits, according to FAO analysis.

For smallholders, improved market access, affordable inputs, and appropriate technology remain fundamental. For commercial operations, proactive financial management, diversification, and operational efficiency provide the margin for survival. For both, policy environments that recognize agriculture's role in food security, employment, and environmental stewardship—rather than treating it as just another sector—will determine whether farming remains viable for the next generation.

Key Takeaways

673 million people face hunger globally; food insecurity is highest in rural farming communities (32%)

Smallholder farms (<2 ha) represent 84% of farms and produce 35% of global food, yet face declining productivity

Agricultural disasters have cost $3.26 trillion over 33 years—Africa loses 7.4% of agricultural GDP to disasters

Global food prices projected to fall 6-7% in 2025, compressing farm margins further

Diversification, market access, climate adaptation, and financial management are universal survival strategies