A new report from AgFunder and ISF Advisors, backed by the Bill and Melinda Gates Foundation, puts a hard number on what many smallholder farmers already feel in their soil. Climate change is here, the damage is compounding, and the money meant to help farmers adapt is arriving far too slowly.

The report, titled Climate Capital: Financing Adaptation Pathways for Smallholder Farmers, estimates that developing countries alone will need around $212 billion a year by 2030 to fund climate adaptation. Today's flows are nowhere near that. Global adaptation financing reached a record $63 billion in 2021 and 2022, but mitigation (the work of cutting emissions) still grew faster, and mitigation still receives roughly 90 percent of all climate finance.

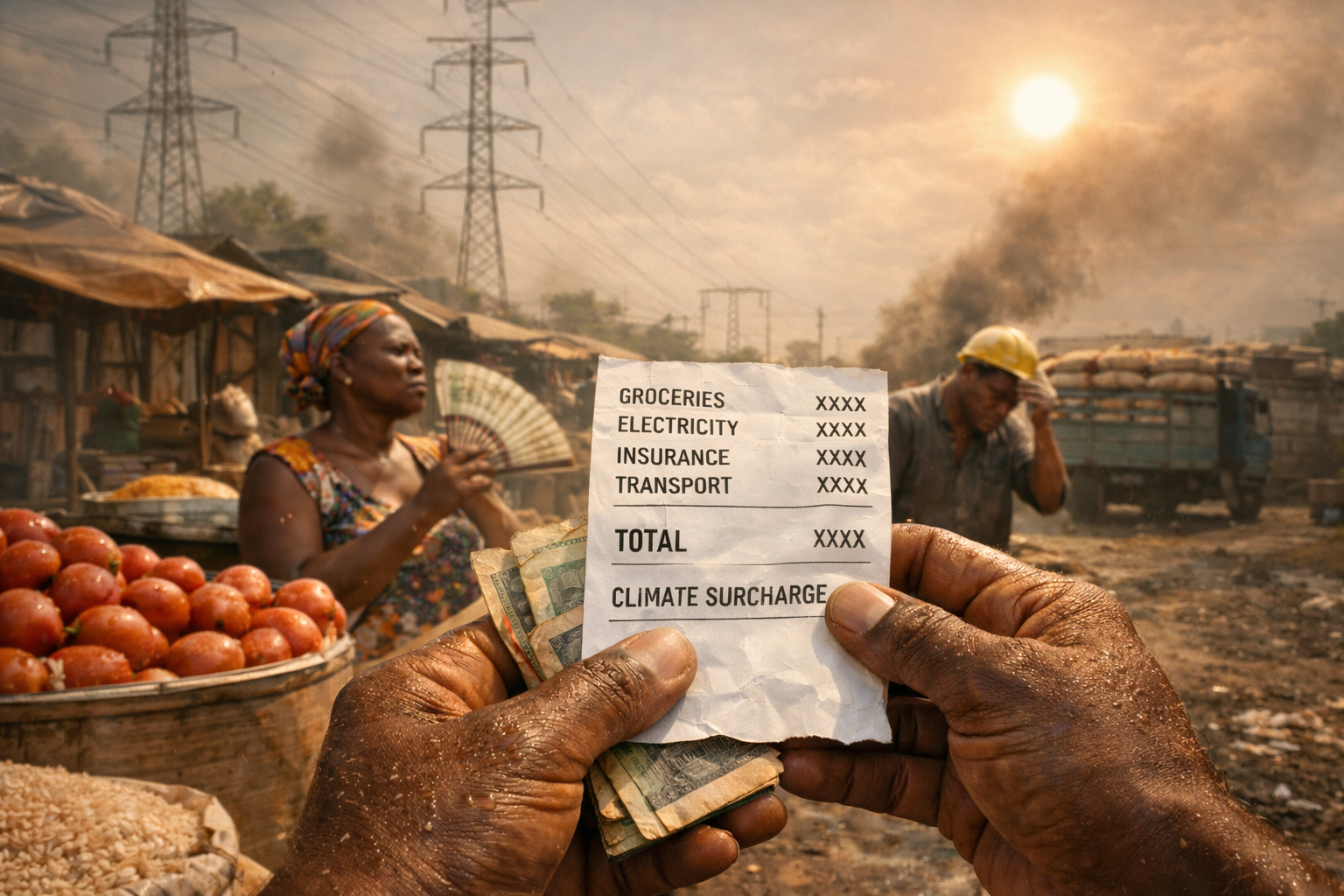

For the world's 500 million smallholder farmers, who produce a third of the food we eat, the gap is not abstract. It shows up as dry maize stalks, flooded rice paddies, and livestock that cannot take the heat. In Sub-Saharan Africa, land responsible for 70 percent of crop value is expected to fall into extreme heat stress by 2050. Global corn and wheat yields could drop by as much as 24 percent and 17 percent respectively as early as 2030. And according to the Global Center on Adaptation, the cost of inaction in Sub-Saharan Africa is roughly $201 billion a year, more than thirteen times the $15 billion needed to act.

Where the money is actually flowing

Despite the shortfall, the report makes clear that adaptation is not an uninvestable theme. It is an underfunded one. Since 2012, venture capital, private equity, and impact investors have put more than $5.7 billion into agrifoodtech startups building tools relevant to smallholder farmers. Funding grew steadily year over year until 2023, when the wider venture market cooled.

India topped the list of countries receiving adaptation tech investment, with $1.9 billion, followed by Israel and Indonesia. Kenya came in fifth at $213 million, and Nigeria rounded out the top ten with $123 million. That is a modest footprint for Africa relative to need but a signal that investors are beginning to look.

The categories drawing the most capital tell their own story. Digital agribusiness marketplaces led with $1.7 billion, as early-stage investors backed platforms that aggregate farmers to unlock better inputs and better markets. Farm management software followed, and fintech came in third, reflecting a broader bet on digital infrastructure as the scaffolding for farm resilience.

Six opportunities worth watching

The authors identify six investable areas where private capital can accelerate adaptation for smallholder farmers:

On-farm and post-farm infrastructure, such as solar irrigation, cold storage, and drying equipment.

Data and intelligence tools, including precision agriculture, traceability, and agroclimatic risk platforms.

Adapted inputs, from heat-tolerant seeds to soil-restoring biologicals.

Financial services, particularly credit and insurance products built for climate-exposed farmers.

Climate-adaptive value chain actors, such as agro-processors who can train and equip the farmers in their supply sheds.

Agricultural marketplaces that connect smallholders to buyers, inputs, and services they otherwise cannot reach.

Each of these already draws commercial interest. None is at the scale the moment demands.

Why public money still matters

The report is direct about one limit of private capital. It rarely moves first. To date, 95 percent of climate finance for small-scale agriculture has come from the public sector, and roughly 14 percent of the adaptation startups in AgFunder's dataset received a grant before any private investor arrived. Blended finance structures, technical assistance facilities, and coordinated government programs remain essential.

Rwanda offers an example worth copying. Its Ireme Invest program channels donor, development bank, and private money through the Development Bank of Rwanda and the Rwanda Green Fund, giving green businesses a single point of entry rather than the usual maze.

What it means for East Africa

For farmers in Kenya, Uganda, Tanzania, and beyond, the takeaway is both sobering and useful. Adaptation finance is growing, and the region is climbing onto more investors' maps, but the pace has to quicken. Digital platforms, better inputs, stronger post-harvest infrastructure, and access to credit and insurance are no longer luxuries. They are what the next decade of farming will require.

The authors close with a plain statement. Adaptation is a readily investable theme. What it needs now is more investors willing to treat it like one.

Based on "Climate Capital: Financing Adaptation Pathways for Smallholder Farmers" by AgFunder and ISF Advisors, supported by the Bill and Melinda Gates Foundation.