When news broke in April 2026 that Microsoft was reportedly slowing its carbon removal purchases, a familiar wave of unease swept through the climate community. It was a small ripple in corporate strategy, perhaps, but one with outsized meaning. Microsoft is estimated to account for around 90% of all carbon removal credit purchases globally, so any shift in its appetite is enough to shake an entire market.

The company has since clarified that its carbon removal program is very much alive and that any change in pace reflects a more disciplined approach rather than a retreat from ambition. Still, the rumor reopened a debate that has divided scientists, businesses, farmers, and policymakers for more than a quarter of a century. Are carbon markets a serious tool for fighting climate change, or are they an elaborate accounting exercise that lets the world's biggest polluters keep polluting?

A Decade of Promises, A Growing Dose of Doubt

In the ten years since the Paris Agreement was signed, public climate commitments have flooded boardrooms and annual reports. Multinationals have purchased credits in the millions, while food and agriculture companies, large and small, have lined up behind frameworks like the Science Based Targets initiative to commit to emissions reductions.

But alongside that wave came another. Greenwashing accusations, investigative reports, and growing skepticism that the climate impact being claimed was anywhere near the climate impact being delivered. Public enthusiasm has cooled, and many corporates have quietly scaled back the loudest parts of their sustainability messaging.

And yet the math hasn't changed. Humanity emits roughly 50 billion tons of greenhouse gases each year, around 38 billion of which is CO₂. Removing carbon from the atmosphere at a meaningful scale is no longer optional. The question is whether markets, as currently designed, can actually do the job.

The Quality Problem That Won't Go Away

The credibility crisis around carbon credits is not a story of a few bad apples. Researchers increasingly describe the problems as systemic. Additionality (would the emissions reduction have happened anyway?), leakage (did the protected forest just shift the chainsaws elsewhere?), double counting, weak verification, environmental injustice, and permanence (will the carbon stay stored for decades or burn up in next year's wildfire?).

A widely cited 2023 investigation by The Guardian, conducted with academic researchers and the journalism nonprofit SourceMaterial, suggested that the vast majority of rainforest carbon offsets approved by Verra, one of the world's largest certifiers, were essentially worthless. The report claimed many protected forests were never genuinely under threat. Verra strongly disputed the findings, but the investigation ricocheted through the industry and triggered a broader reckoning.

The 2022 FIFA World Cup in Qatar offered another headline case, with organizers claiming the tournament would be the first "fully carbon-neutral" edition. A formal complaint backed by several European consumer authorities later found the claim misleading, citing underestimated emissions and questionable offsets.

The pattern is uncomfortably familiar. When a market rewards low prices over verified impact, smart actors with weaker scruples will always find ways to game it.

Signals of a Maturing Market

Not everyone is ready to write off the system. A growing camp of practitioners argues that carbon markets are finally maturing. Slowly, painfully, but genuinely.

The Integrity Council for the Voluntary Carbon Market (ICVCM), which emerged in 2021 from the Taskforce on Scaling the Voluntary Carbon Markets (TSVCM), was designed to be the referee the industry never had. Its Core Carbon Principles (CCPs) act as a quality benchmark, and credits that earn the label are increasingly treated as the gold standard.

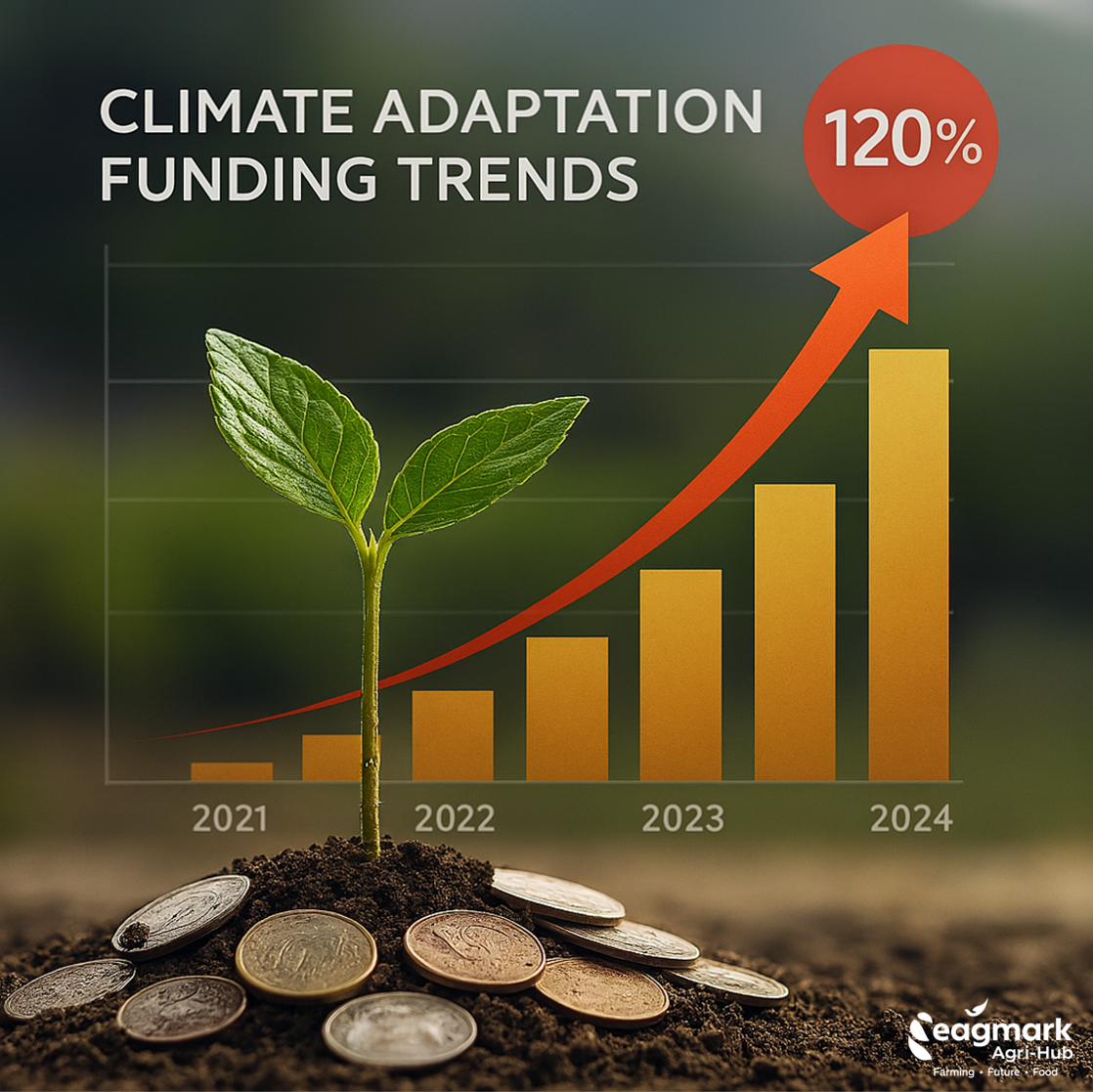

In late 2025, soil carbon credits issued by U.S. agtech firm Indigo Ag, through its Carbon by Indigo program, became the first agricultural credits to receive CCP certification. Indigo, which is now on its third major carbon agreement with Microsoft (a 12-year deal announced in January for 2.85 million credits), has framed the milestone as proof that soil carbon can be done at scale, with rigor.

For the farmers generating those credits, the label matters less as a marketing tool and more as a guarantee that the work they are doing in their fields will be recognized and paid for by the market.

A similar shift is unfolding in Europe. Danish soil carbon marketplace Agreena reports that methodologies considered acceptable just three years ago are now ineligible for sale on its platform. Agreena calculates credits based on the carbon a farmer captures through practices like cover cropping, reduced tillage, and organic fertilization, then helps growers sell directly to buyers (taking a 15% broker fee). Credits, by this view, are quietly transforming from cheap excuses into integrity-based instruments where the supply side actually has to prove what it claims.

The "Medieval Indulgences" Critique

Other voices in the regenerative agriculture movement remain deeply unconvinced. Amfora, a European retailer working with regenerative olive oil producers, has refused to participate in carbon markets entirely.

Its reasons are both practical and philosophical. Practically, the financial benefit to a small farmer is often negligible, equivalent to nudging the price of a bottle of olive oil up by 2%. Philosophically, the critique cuts deeper. Selling credits to large corporations that continue polluting elsewhere effectively cancels out the local environmental gains. The metaphor that keeps coming up is that of medieval indulgences. Payments made to feel forgiven without actually changing behavior.

It is a critique the market has not yet fully answered.

Insetting: The Quiet Shift Inside Supply Chains

A third path is gaining momentum. Carbon insetting, where companies fund emissions reductions inside their own supply chains rather than buying offsets from unrelated projects.

German agtech startup Klim, which works with farmers across Europe to adopt regenerative practices, has built much of its business on this model. For agrifood multinationals, the approach directly tackles Scope 3 emissions, the hard-to-track emissions outside a company's direct operations, which often represent the bulk of an agrifood company's footprint.

Insetting also has a business case that offsetting has always struggled to make. Investing in regenerative practices among the farmers who actually grow your ingredients tends to improve the long-term reliability of supply, reduce climate-related disruption, and build resilience into a P&L. With staple crops like cocoa, coffee, bananas, wheat, and maize all under increasing climate stress, more food companies are quietly approaching this work as risk management rather than philanthropy.

It also begins to address the permanence question. Real soil carbon work requires long-term agreements, multi-year commitments to farmers, not one-off purchases. And it raises a question the industry is only starting to grapple with. What happens when a farm changes hands? How is decades-long investment in soil health protected across generations of ownership?

What's Actually Missing: Accountability

For all the heat in the debate, there is broad agreement on one thing. Carbon markets are not going away. The world has too much CO₂ in the atmosphere and too few tools to remove it. Some categories of climate projects, including clean cookstoves and landfill gas capture, have a credible path to robust verification.

What is missing is what every functioning market eventually develops. An independent, enforceable system of oversight. Imagine a stock exchange with no regulator. Anyone could issue shares. Prices would collapse to whatever the least scrupulous seller offered. Buyers would have no way of knowing what they actually owned.

That, critics argue, is roughly where carbon markets sit today. Brokers know that if they refuse to certify a weak project, someone else will. Without a referee, the market drifts toward the cheapest credit rather than the most credible one. A textbook case of Gresham's Law, where bad money drives out good.

A cheap thing isn't necessarily worthless. But when carbon credits trade at average prices of $2 or $3 a ton, the math becomes unforgiving. If solving the climate crisis were really that cheap, the world would have solved it long ago.

The Decade Ahead

The next phase of carbon markets will likely be defined less by ambition and more by accountability. Regulators are circling. Buyers are getting more careful. Standards bodies like the ICVCM are tightening. Farmers, finally, in some places, are beginning to see real money for real work.

Whether that's enough to move the climate needle is another question entirely. But the era of buying one's way to a clean conscience for the price of a coffee is, slowly, coming to an end. What replaces it will determine whether carbon markets become a serious instrument of the energy transition or another well-intentioned chapter in the long history of climate promises that didn't quite add up.